![]()

Could the Apple Watch Series 4 Be as Successful as the iPhone?

Follow Brett on Twitter @wintonARK

Apple surprised the market this week with the first FDA-approved electrocardiogram for sale to end-consumers: it embedded that capability into its fourth generation Apple Watch, which is thinner, faster, and larger than its predecessors. While previous generations of the Watch could notify wearers of suspicious pulse-rate changes, Apple has closed the loop by empowering users to forward EKG results to medical professionals. Adding to its utility, the Apple Watch can detect falls and contact emergency services if a person is unresponsive, suggesting that it is transitioning from a nice-to-have device to a necessity for certain demographics, particularly the elderly. While 10% of iPhone buyers have purchased an Apple Watch historically, its new life-saving features should increase the cross-selling opportunity substantially.

With these advances, Apple is preparing for a wide scale deployment of its Watch that could mirror that of the iPhone. Initially, consumers paid only $200 for the iPhone, as its telecom partners picked up the majority of the tab, $650. As a result, the iPhone was a cashflow hit for both Apple and the telecom operators. iPhone owners were willing to pay for much more data than historically had been the case, and Apple sold more than a half-trillion dollars-worth[1] of devices before AT&T ended its subsidy in early 2016.

Health insurance providers could become to the Apple Watch what telcoms were to the iPhone. If patients wearing an Apple Watch were to incur health costs substantially lower than others, insurers probably would be willing to subsidize its use. Simple math suggests that success on just one indication—atrial fibrillation—could incentivize insurance companies to give everyone in the US over the age of 40[2] an Apple Watch for free. While insurers probably will proceed cautiously, collecting data to make sure that the economic case is sound, pilot programs already have startedwithout EKG capability, suggesting that FDA approval will accelerate the trend.

[1] Company reports (Apple, AT&T); ARK estimates.

[2] The lifetime annual medical cost burden of strokes for people over age 40 in the US comes to roughly $100 billion and approximately 20% of those strokes are attributable to Atrial Fibrillation (AF). Early diagnosis of Atrial Fibrillation reduces stroke-risk by 2/3rds, so if the Apple Watch were consistently capable of diagnosing Atrial Fibrillation (and had no other health benefit) then insurers would see a 5-year savings of $70 billion; they could by everyone in the US over the age of 40 an Apple Watch for $60 billion. This calculation is intended to be indicative of potential performance; all numbers are roughly representative of root truth.

What Are the Trade-Offs for Enhanced Technological Capabilities of Cryptonetworks?

Follow Yassine on Twitter @yassineARK

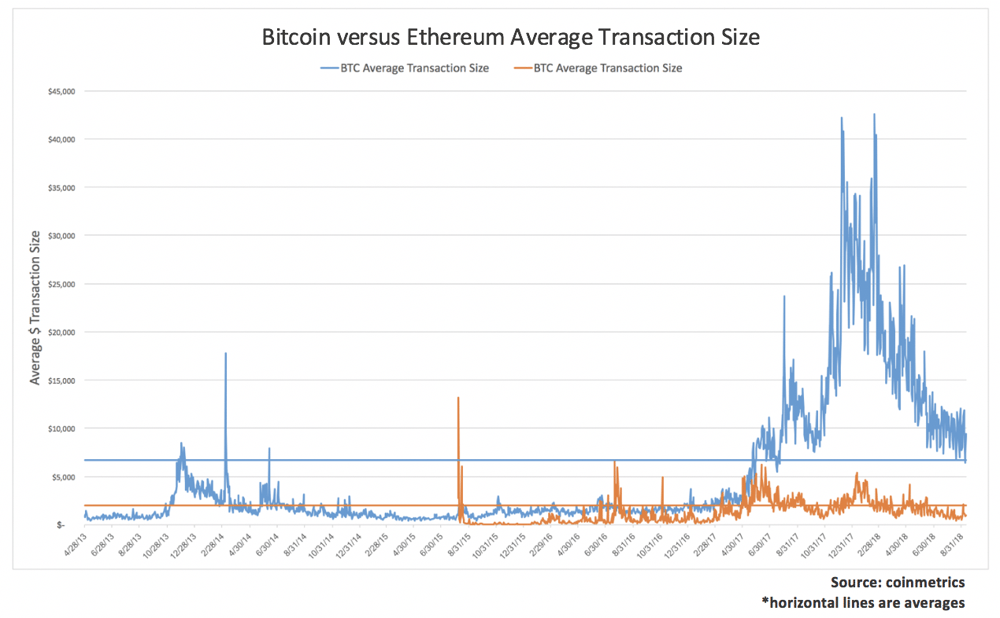

As ARK's research has shown Bitcoin’s annual throughput capability at the base layer is several orders of magnitude below any existing payment system, but other metrics are putting that metric into an interesting perspective. As measured by annual transactions value, Bitcoin’s base layer is supporting two times the throughput of Paypal today and is within an order of magnitude of Visa’s throughput. In other words, the use case for Bitcoin’s base layer as a settlement network for large transactions is real and growing.

Increasingly, a cryptonetwork’s technological capabilities seem to come at the cost of other features, such as security, censorship resistance, and the predictability of money supply. Aiming to be a global non-sovereign monetary store of value, bitcoin would not want to see advancements in its technological base layer occur at the expense of censorship resistance, security, or money supply. Alternatively, a cryptonetwork like Ethereum, aiming to provide trustless and decentralized computation, might prioritize technological capabilities over the other variables.

A common metric used for measuring technological capability and blockchain scalability is transactions per second. Given the goals of various cryptonetworks and the tradeoffs they are willing to accept, Bitcoin should and does support lower transaction counts than Ethereum, as shown below.

At the same time, while Ethereum supports higher average transaction counts, Bitcoin should support greater value per transaction given its use case as a settlement layer for large value transactions. Such is the case, as shown in the graphs depicting both total transaction value and average transaction size below.

Will Challenger Banks Deliver Real Value to Consumers?

Follow Bhavana on Twitter @bhavanaARK

Challenger banks are “challenging” traditional banks. Typically, their go-to-market strategy is online and mobile, allowing them to offer competitive pricing and a better user experience. Chime, Simple, N26, and Varo Money are notable startups in this space.

More than 100 challenger banks worldwide have attracted significant venture capital investments. Most of these banks have targeted low-income and underserved demographics which, in the US, account for only 7% of households. To address the middle- and high- income end of the market in the US and elsewhere, these startups are trying to overcome customer inertia associated with moving from traditional checking accounts by competing on pricing and interest rates. In the US, for example, challenger banks are offering an average deposit rate of 0.79%, three times more than traditional banks.

Competition on price basis does not qualify as disruption innovation. Instead disruptive companies need to leverage technology, offering products and experiences that are inherently different from the existing world order.