|

|

|

|

|

|

|

|

|

![]()

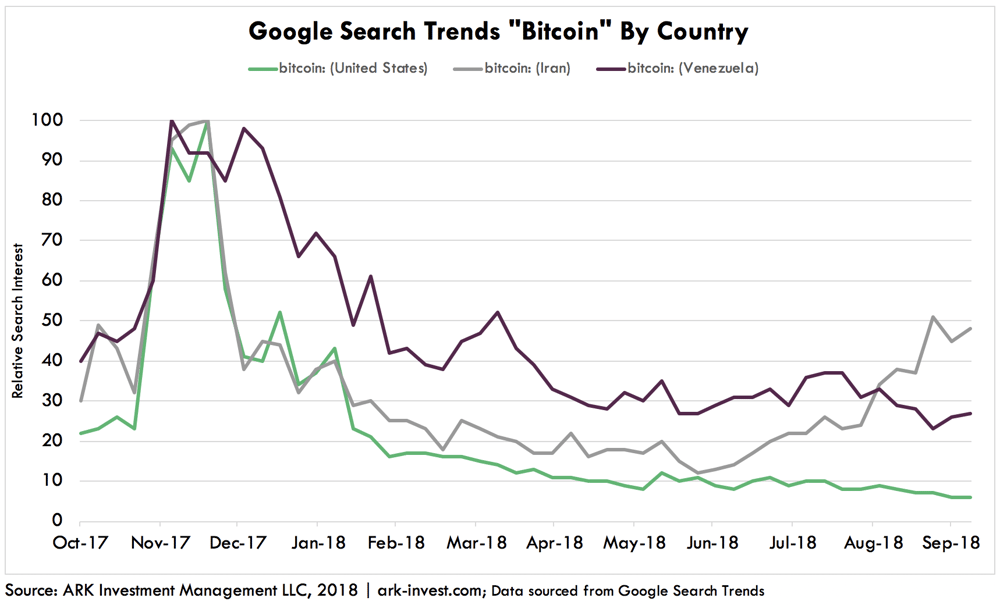

Google Search Trends Speak Volumes About Bitcoin Demand

Follow Yassine on Twitter @yassineARK

In the past, ARK has hypothesized that cryptocurrencies could accelerate the spread of financial crises in emerging markets. As monetary authorities in emerging markets lose control of inflation, their populations will lose confidence in their fiat currencies and search for alternative stores of value, like bitcoin. As the financial crisis evolves, businesses gradually will accept bitcoin for payment until, ultimately, they demand it exclusively as inflation evolves into hyperinflation.

Already, the Google Search Trend for “bitcoin” shows more searches in emerging markets experiencing hyperinflation, like Venezuela and Iran, than in much larger developed countries like the United States, as shown below. In addition to exchange volumes, this indicator could be an effective proxy for bitcoin demand in hyperinflation-prone countries.

Toward the end of 2017, the value of all cryptoassets peaked at more than $800 billion, as bitcoin’s price hit nearly $20,000. Around the world, the bitcoin price and Google searches for bitcoin hit peaks at roughly the same time. After the large sell off in prices this year, however, Google Search Trends in the US declined significantly, while those in countries like Iran and Venezuela fell less and have trended up in the last couple of months. Perhaps the demand for bitcoin in the US has been speculative and more highly correlated to price, while in the emerging markets it has been stoked by the desperate need for an alternative store of value.

Is Bitcoin Unflappable?

Follow Brett on Twitter @wintonARK

If forecasts a month ago were that US equity market volatility, as measured by the VIX index, was about to break out to its highest point since September of 2015 and that the S&P 500 was going to drop by more than 8%, investors might have responded with a shrug. After all, equity markets go through spells of uncertainty, with earnings reports often causing a reassessment of fundamental assumptions.

At the same time, forecasts of bitcoin’s response to increased equity market volatility probably would have ranged from a rally as a “flight to safety” to a sell-off as another speculative asset. Few, if any would have anticipated what has occurred instead.

Bitcoin has done very little at all.

During the past month, while the S&P 500 lost 8.5%, bitcoin slipped just 0.3%, and while the S&P oscillated by roughly 1% per day on average, bitcoin moved by less than 0.9%. Historically a more volatile asset, bitcoin has been more stable than the equity market during the period.

Bitcoin’s behavior is provocative, suggesting perhaps that equity investors have little, if any, cryptoasset exposure, or that expectations for bitcoin prices are independent of expectations for other assets’ prices. Efficient portfolio theory suggests that investors should seek to diversify a portfolio with independent bets so that an asset that holds its value in a turbulent environment, against expectations, captures more attention, even from skeptics.

Though bitcoin’s volatility will jump again at some point, if it were to do so while other assets have calmed down, then its role as part of a new asset class would make it all the more interesting to both retail and institutional investors.

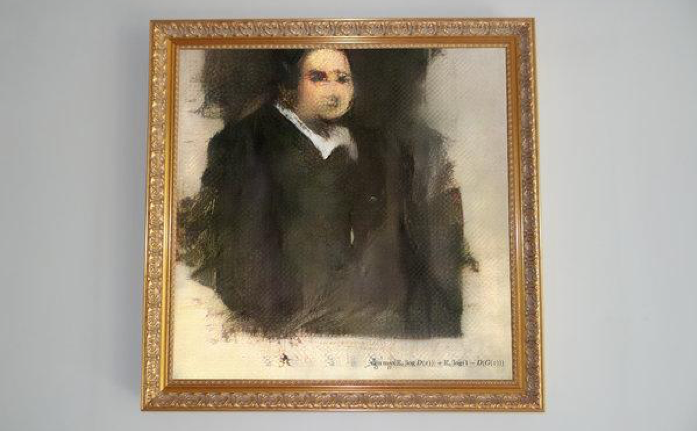

AI Art Fetches $432,500 at Christie’s Auction

Follow James on Twitter @jwangARK

This week, Christies auctioned a painting created by a neural network for more than $400,000, exceeding the price paid for Warhol and Lichtenstein pieces sold the same day. The public’s growing interest in this novel technology may have helped the piece fetch an unprecedented price.

Obvious, a French art collective founded by three students, created the painting based on the source code of Robbie Barrat, a 19 year old researcher at Stanford who has used artificial intelligence (AI) to create art, anywhere from landscapes to nudes.

The use of AI in art goes back decades. New in this case, however, is the application of Generative Adversarial Networks (GANs), a neural network able to imitate. Invented just five years ago by Ian Goodfellow, GAN’s rapid evolution from a research project to a cultural awakening speaks volumes about the accelerating pace of AI adoption.

|

|

|

|

|

|

|

|

CRISPR’s Coverage Area Has Increased

Follow Manisha on Twitter @msamyARK

CRISPR genome-editing technology has emerged as a versatile biological tool that potentially could cure debilitating diseases, diagnose infectious diseases, and unlock secrets to basic biology, including how cells function.

CRISPR-Cas9 derived from S. pyogenes (CRISPR-SpCas9)has been the most widely studied technology upon which the first US CRISPR clinical trials have been based, but it does have some significant shortcomings. SpCas9 is a “nuclease”, an enzyme that edits the human genome by cutting DNA or RNA but requires the target to be flanked by a sequence known as the protospacer adjacent motif (PAM). The PAM sequence can be thought of as a zip code. The postal carrier, CRISPR, can edit DNA or RNA only in the zip codes in its coverage area.

Scientists at MIT have discovered a new Cas9 protein derived from S. canisbacteria (ScCas9) with a larger coverage area, or zip code, than SpCas9. While SpCas9 addresses only 9.9% of the human genome, ScCas9 can deliver to nearly 50%, with a 1.5-fold decrease in off-to-on target ratios, suggesting better accuracy and safety.

While this discovery is a significant step forward for CRISPR, ScCas9 will not displace SpCas9. In many instances, inactivating a gene is sufficient to correct a disease and its symptoms, as the average size of a gene is 10-15,000 base-pairs of DNA, a region broad enough for SpCas9 to address. ScCas9 will work better with point mutations, diseases caused by a single base error and requiring a correction rather than a gene disruption.

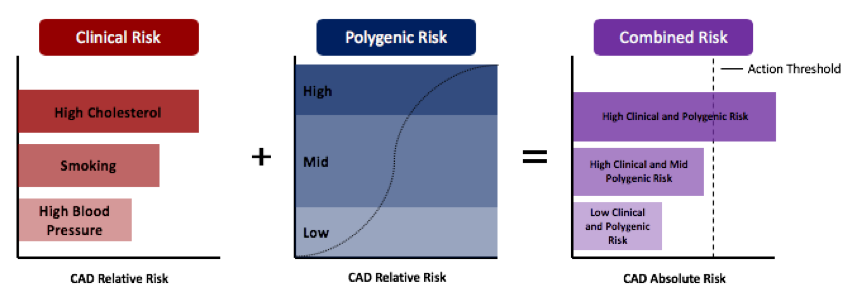

The Clinical Adoption of Polygenic Risk Scores Has Been Slower Than Expected

Follow Simon on Twitter @ARKInvest

Polygenic risk scores (“PRS”) have not lived up to expectations in the clinic. These diagnostic tests seek to quantify the risk of developing a disease by running a statistical regression on the structural variants found in a patient’s genetic code.1 Those with risk variants associated with a disorder will be at higher risk than those without the variants.1 Thus far, the integration of risk scoring with other diagnostic tests has been slowed by the complexity of polygenic diseases and the lack of population-specific reference genomes.1,2 That said, while they won’t replace traditional tests such as high blood pressure or cholesterol in the short term, PRS tests could serve as useful complements.

Figure 1: Deriving absolute risk for patient risk-stratification may incorporate an analysis of traditional risk factors and the results of a polygenic test.2 Figure 1: Deriving absolute risk for patient risk-stratification may incorporate an analysis of traditional risk factors and the results of a polygenic test.2

Innovations in neural networks, statistical models, and high-throughput DNA-sequencing are increasing the accuracy of polygenic risk scores.1,3 A recent publication by Khera et al. illustrates how these innovations will enhance the clinical utility of the PRS.4 The genome-wide polygenic score for coronary artery disease (CAD) proposed in this study (“GPSCAD”), for example, scored patients at risk of contracting CAD from low to high, pushing the highest odds on average from 1.4 times normal in traditional tests to 5 times with PRS.4 The difference in this risk multiple should become clinically actionable.

The US Preventive Services Task Force, for example, recommends that those aged 40-75 years with risk factors like obesity, smoking, and/or high cholesterol should be on a low to moderate dose of statins.2 Introducing a CAD PRS could help physicians prescribe and accelerate treatment plans.

Sources:

1. Kilpinen, H., & Barrett, J. C. (2013). How next-generation sequencing is transforming complex disease genetics. Trends in Genetics, 29(1), 23-30. doi:10.1016/j.tig.2012.10.001

2. Torkamani, A., Wineinger, N. E., & Topol, E. J. (2018). The personal and clinical utility of polygenic risk scores. Nature Reviews Genetics, 19(9), 581-590. doi:10.1038/s41576-018-0018-x

3. Luo, R., Lam, T., & Schatz, M. (2018). Skyhawk: An Artificial Neural Network-based discriminator for reviewing clinically significant genomic variants [Abstract]. BioRxiv. doi:10.1101/311985

4. Khera, A., Chaffin, M., Aragam, K., Haas, M., Roselli, C., Choi, S., . . . Kathiresan, S. (2018). Genome-Wide Polygenic Scores for Common Diseases Identify Individuals with Risk Equivalent to Monogenic Diseases. Nature Genetics. doi:10.1038/s41588-018-0183-z

|

|

|

|

|

|

|

|

|

|

|

|

|