Please enjoy ARK's weekly newsletter curated by our thematic analysts and designed to keep you engaged with disruptive innovation. Have a wonderful day!

Waymo Reintroduces Human Safety Drivers to Its “Autonomous” Fleet

This week, The Information reported that Waymo is reintroducing safety drivers to its autonomous vehicle prototypes in Phoenix, a clue that it may not launch commercial service this year after all. Last November, Waymo became the first company to remove safety drivers from its autonomous cars, but now CEO John Krafcik says that its autonomous taxi service may include safety drivers and may not be available to the general public when it launches. Waymo had planned to launch commercial service before the end of 2018, so these reports suggest some rethinking.

The Information also highlighted some of the challenges Waymo’s vehicles are encountering, including navigating during peak shopping hours at Walmart and yielding unnecessarily to other vehicles at highway onramps. Interestingly, Tesla recently introduced Navigate on Autopilot which is enabling autonomous driving onto and off of highway entrances and exits.

Waymo and Tesla are tackling autonomous driving from different angles. First, while Waymo started training on suburban streets, Tesla focused on highways. Second, Waymo’s autonomous driving strategy is “deterministic”, trained with highly detailed maps, while Tesla’s is “probabilistic”, trained on short videos of myriad driving scenarios generated from its customers’ vehicles. Waymo uses LiDAR and a number of radar and camera sensors, enabling a highly accurate perception system, while Tesla uses no LiDAR and fewer radar and camera sensors, perhaps a less robust perception system but one with significantly more focus on path planning from point A to point B.

Waymo’s highly sensitive sensor suite could be causing overkill, with too much information causing decision-making challenges and gridlock. Whether or not it occurs within the next four weeks, its commercial launch should provide some important insights on the strengths and weaknesses of deterministic and probabilistic autonomous driving strategies.

Counterintuitively, Automation Should Increase the Number of Food Service Jobs

Although calls to automate an industry often cause fears of unemployment, history shows that robots can and do create jobs. Two mathematical relationships explain how automation can increase employment: productivity gains relative to the price elasticity of demand, and the shift from non-paid to commercial activity.

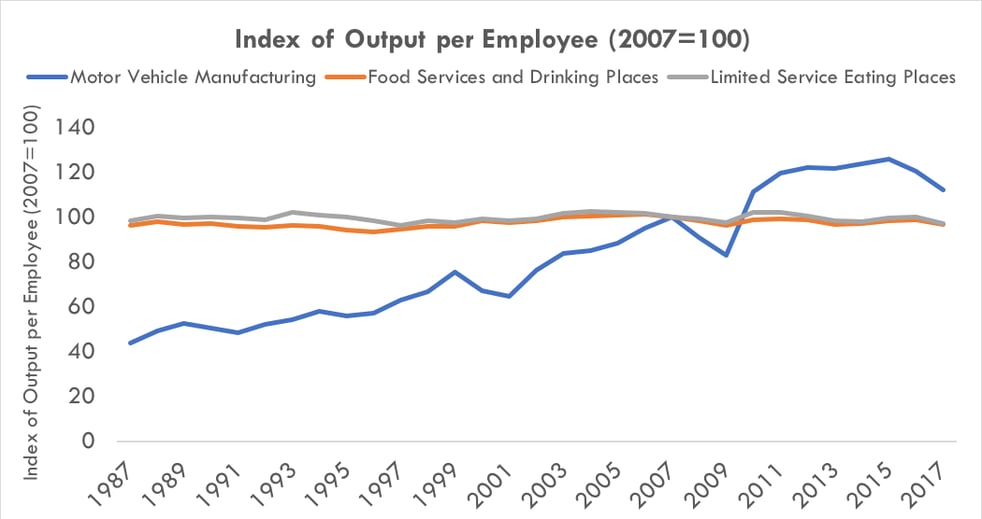

Productivity in the food services industry has been relatively flat for the past 30 years, quite a contrast to that in the motor vehicle industry which has nearly tripled, as shown in the chart below. At the same time, employment in the US auto industry has increased fairly consistently. The food service industry could be on the threshold of the same dynamic.

Automation should lower the cost of delivering food services, increasing the demand not only for out-of-home meals but also for robots and labor. As long as the price elasticity of demand for out-of-home food services is higher than the productivity gains associated with automation, this relationship should hold true.

Also increasing employment should be the shift from in-home to out-of-home meal preparation, pushing “non-market activity” into the commercial market and the labor statistics. According to the Bureau of Labor Statistics, the value of food consumed in-home in the US is $700 billion, approximately the same as the $700 billion spent on food prepared outside of the home.

Not included in these statistics is the value of preparing for and cleaning up after meals at home. In the US, the time spent prepping for and cleaning up after meals is roughly 36 minutes per person, or $6.60, per day which, when applied to the number of US adults, amounts to roughly $700 billion. As automation lowers the cost of eating out (or ordering in), more consumers will shift their spending from supermarket to restaurants, pushing “non-market activity” into the market.

Source: ARK Investment Management LLC, Bureau of Labor Statistics

OFAC sanctions Bitcoin addresses. But how effective can these sanctions actually be?

This week, the Treasury Department’s Office of Foreign Assets Control (OFAC) announced that, for the first time, it is adding two Bitcoin addresses to its Specially Designated Nationals list. "As part of its enforcement efforts, OFAC publishes a list of individuals, groups, and entities, such as terrorists and narcotics traffickers, designated under programs that are not country-specific. Their assets are blocked and U.S. persons are generally prohibited from dealing with them." The two owners of the addresses had facilitated ransom payments for Iranian cyber attackers.

OFAC's Bitcoin address blacklisting has sparked debate as to whether or not it will be enforceable technologically. In a recent thread, LaurentMT lays out the two restrictions necessary for the blacklist to be effective on the Bitcoin blockchain.

One of the sanctions restricts individuals from accepting any transactions from the blacklisted address. "As a push system", however, Bitcoin renders this restriction unenforceable: as long as an address is valid and publicly available, no entity can restrict a user from sending bitcoin to it. Instead, the restriction could taint an honest wallet if it were to receive bitcoin from the blacklisted address.

Alternatively, sanctioning could restrict individuals from sending transactions to the blacklisted address. While seemingly more enforceable, privacy features like Coinjoin in the Bitcoin network suggest otherwise. With Coinjoin, tracking and identifying individual senders and receivers is very difficult, as shown below.

If Dave's address were to be sanctioned, for example, Bob would face criminal charges for sending him bitcoin. With Coinjoin, however, identifying the sender would be much more difficult, as shown on the right diagram above. Is the sender Bob or Alice?

While Bitcoin’s transparency and traceability has aided governments to crack down on criminal activity thanks to help from cryptographic experts, enforcing sanctions such as those from OFAC on an underlying public blockchain could prove to be much more nuanced and difficult.

Amazon Web Services Is The Everything Store For Enterprise Computing

While Amazon calls its consumer-facing business The Everything Store, Amazon Web Service (AWS) is becoming the everything store for enterprise computing. Its Reinvent developer conference last week made that point clear.

The most notable announcement was Amazon’s hybrid cloud service called Outposts. Since its inception, Amazon has focused AWS on the public cloud, a service that allows any company to rent computing power and storage from Amazon’s data centers. Competitors like Microsoft and IBM have offered hybrid cloud services which manage an enterprise's existing data centers and offer pay-as-you-go services in the cloud. With Outposts, Amazon is embracing the hybrid cloud for the first time: Amazon not only will rent as many servers as an enterprise needs, but also will sell, install, and manage servers in an enterprise's own data centers. Microsoft, Dell, Cisco, and HP had better watch out.

Not content with disrupting enterprise computing, Amazon also intends to displace chip makers. At ReInvent, it announced two chips, it’s own ARM based server processor called Graviton and an artificial intelligence inference chip dubbed Inferentia. At its scale, Amazon no longer needs to cede profit margins to Intel and Nvidia: it can design its own chips. Neither company will be replaced any time soon but, clearly, in the cloud era chip makers will be competing not only against each other but also potentially against their customers.

Amazon's announcements this week ranged from databases to machine learning services and could fill an entire newsletter. In other words, AWS is emerging as the everything store—for enterprise computing.

The Cost Decline of Short-Read Sequencing Could Fuel Clinical Adoption

Spread by pathogenic microorganisms like bacteria, viruses, and parasites, infectious diseases account for roughly 19% of global deaths. Discovering the source of these infections involves culturing blood samples, which provides limited if any information and requires weeks of turnaround time. Meanwhile, patients have to take antibiotics which can be ineffective and can cause serious side effects.

In the face of barriers to adoption, clinical metagenomics are beginning to benefit from biochemical breakthroughs. Oftentimes, most of the DNA in a sample is the patient’s, obfuscating the source of the infection. Increasingly, the selective depletion of host DNA and the amplification of microorganismal nucleic acids are solving that problem, as are robust bioinformatics tools that leverage artificial intelligence. ARK believes that over the next five years, the cost to sequence a whole human genome will fall to $100 (USD), accelerating the cost-effectiveness of metagenomics and spurring the growth of personalized antibiotic therapies.

On the eve of the International Summit on Human Genome Editing, Chinese scientist Jianku He shocked the scientific world by disclosing the birth of twin girls whose embryo’s had been edited using CRISPR. He also announced that another CRISPR baby is on the way.

Using CRISPR, Dr. He mutated the CCR5 gene, which is tied to HIV-resistance, in embryos and then implanted them into the mother. While the father of the twins was HIV-positive, the goal of the procedure was to confer lifetime HIV-resistance. Dr. He "washed" the sperm to ensure that the embryos would be HIV-negative, triggering ethical concerns that the gene-edit was not addressing a high unmet need.

Dr. He claims that the twins are healthy, though his claims have not been peer-reviewed. Questions now include whether or not the twins’ identities should remain private, as they will have to be monitored throughout their lifetimes.

Dr. He had studied at Stanford University and may have conceived of the CRISPR trial at Rice University with his mentor, Michael Deem. He and Deem now are under investigation for ethical misconduct and endangering patients. In addition, China has banned germline editing studies.

The US prohibits embryonic germline editing and scientists around the world have agreed that, while it will be permissible in circumstances of “high unmet need” with no reasonable alternatives at some point in the future, germline cells should not be edited, yet. Germline edits are inheritable, passed down to future progeny. Ironically, Dr. He was involved in proposing the first human gene-editing regulations in 2015.

ARK's statements are not an endorsement of any company or a recommendation to buy, sell or hold any security. For a list of all purchases and sales made by ARK for client accounts during the past year that could be considered by the SEC as recommendations, click here. It should not be assumed that recommendations made in the future will be profitable or will equal the performance of the securities in this list. For full disclosures, click here.

You received this email because you are subscribed to Research NewslettersfromARK Investment Management LLC. Unsubscribe from ARK emails or choose the types of emails you want to receive. Unsubscribe from all.

This Newsletter is for informational purposes only and does not constitute, either explicitly or implicitly, any provision of services or products by ARK Investment Management LLC (“ARK”). Investors should determine for themselves whether a particular service or product is suitable for their investment needs or should seek such professional advice for their particular situation. All content is original and has been researched and produced by ARK unless otherwise stated therein. No part of the content may be reproduced in any form, or referred to in any other publication, without the express written permission of ARK. All statements made regarding companies, securities or other financial information contained in the content or articles relating to ARK are strictly beliefs and points of view held by ARK and are not endorsements of any company or security or recommendations to buy or sell any security. By visiting and/or otherwise using the ARK website in any way, you indicate that you understand and accept the terms of use as set forth on the website and agree to be bound by them. If you do not agree to the terms of use of the website, please do no access the website or any pages thereof. Any descriptions of, references to, or links to other products, publications or services does not constitute an endorsement, authorization, sponsorship by or affiliation with ARK with respect to any linked site or its sponsor, unless expressly stated by ARK. Any such information, products or sites have not necessarily been reviewed by ARK and are provided or maintained by third parties over whom ARK exercises no control. ARK expressly disclaims any responsibility for the content, the accuracy of the information, and/or quality of products or services provided by or advertised on these third-party sites.