![]()

The Mining Death Spiral Is the Latest FUD Around Bitcoin

Follow Yassine on Twitter @yassineARK

The bear market in bitcoin is breeding fear, uncertainty, and doubt (FUD). Increasingly, arguments against bitcoin that had been debunked are resurfacing.

The latest? Bitcoin mining has entered a death spiral. As Matt Odell first pointed out in June of 2018, "the lowest hanging fruit for the next batch of unsubstantiated FUD will be the ‘mining death spiral’ articles that appear every bear market and halving." The Block's technical analyst, Arjun Balaji, lays the argument for a miner-induced death spiral: "Bitcoin prices drop materially, eventually marginally profitable miners shut off, ad infinitum, until all the miners are gone and no one mines bitcoin."

The inconsistency of this argument lies in Bitcoin's proof of work difficulty adjustment. Proof of work difficulty is a measure of the difficulty to hash a block. Difficulty is set so that, on average, the hash of a block takes roughly 10 minutes. The biggest determinant of the proof of work difficulty is the hash rate of the Bitcoin network which, in turn, is set by the price of bitcoin. Every 2016 blocks, the Bitcoin network reassesses its global hash rate to determine whether the difficulty is consistent with the network's ability to find blocks every 10 minutes.

Earlier this week, Bitcoin's mining difficulty dropped 15%, exceeded only by the 18% drop in November 2011. Causing the sharp adjustment downward in difficulty was a drop in the hash rate as miners left the market in response to lower prices and profits.

Ironically, mining profitability provides the case against a mining death spiral. Miners still in the network after the proof of work difficulty adjustment should garner a larger percentage of the hash rate, increasing their probability of finding and profiting from the next block. We believe higher rewards per block should compensate for the drop in price, rendering the mining death spiral improbable.

Even during a significant drop in the hash rate prior to a difficulty adjustment, game theory suggests that a death spiral would be unlikely as some miners probably would mine at a loss up in anticipation the downward adjustment in difficulty. Their contractual obligations, particularly those associated with equipment, should incentivize miners to mine at a loss until the next difficulty adjustment.

The Arrest of Huawei’s CFO Portends a Cold War Over 5G

Follow James on Twitter @jwangARK

The dramatic arrest of Huawei’s Chief Financial Officer could have ramifications for the emerging 5G market. In recent years, Huawei has surpassed Nokia and Ericsson as the world’s top supplier of telecommunications equipment. Yet, as trade and national security tensions have simmered and flared between the US and China, Huawei equipment has been unable to penetrate US telecom facilities. Security experts fear that Huawei’s close ties to the Chinese government could compromise US networks.

As a result, this summer Congress passed the 2019 National Defense Authorization Act which bans the use of certain Chinese telco equipment in US government agencies. As the global wireless industry begins to transition to the long-awaited 5G technology, Huawei has been aiming to grow its market share and become the global leader. Because western leaders do not want to cede the future of wireless to a Chinese firm, the strong enforcement action against Huawei’s CFO is not surprising.

If Huawei has been evading sanctions and selling telecom equipment to Iran, it could face the same measures that nearly killed ZTE. As a result, Nokia and Ericsson, after a long and painful competitive decline, finally could have the wind at their backs in the 5G wireless technology race.

Japan Aims for a Cashless Economy and Promotes Digital Payments

Follow Bhavana on Twitter @bhavanaARK

According to ARK’s research, cash accounts for roughly 80%, or 1.4 trillion global transactions, annually, with its share in Japan near the top of the range. In Japan, cash is both a means of payment and an asset, thanks to years of a zero interest policy, deposit insurance levels limited to 10 million Yen, and high sales taxes. According to the Bank of Japan, ~50% of the assets held by households are currency and deposits.

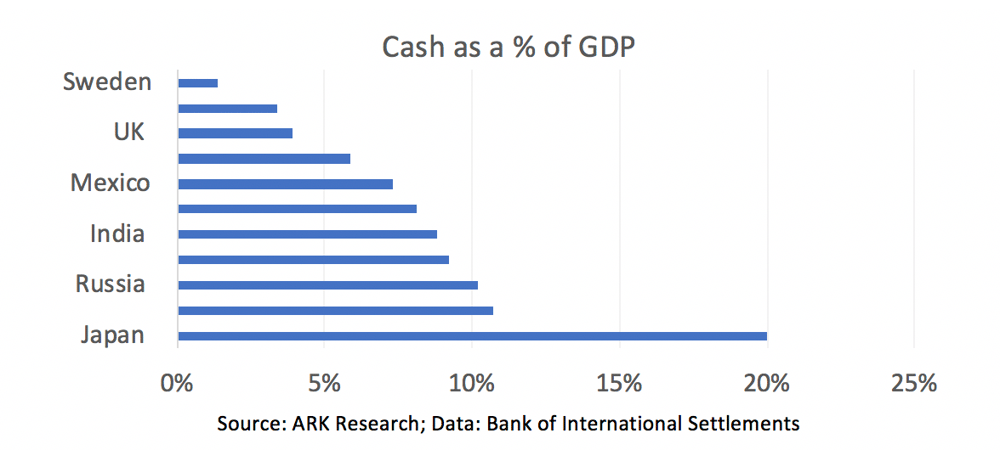

Cash accounts for 20% of GDP in Japan, roughly twice the drag on its economy as that in the US and China, as shown below. To address this issue, the Japanese government has formed a “cashless promotion council” to achieve a digital payment rate of 40%, including several initiatives: 1) the standardization of QR code settlements, 2) consumer education on the benefits of cashlessness, and 3) digital payment data collection.

Companies like Softbank and Line Corporation are moving aggressively to capitalize on these initiatives. Softbank’s digital payment offering called PayPay, run by India’s Paytm, has allocated 10 billion Yen to offer 20% cash back on purchases. Similarly, Line Corporation in partnership with WeChat Pay is offering 3% cash back to attract new customers and serve Chinese tourists in Japan. These digital wallets will benefit not only from transaction fees but also advertising revenues and the potential to become “personalized bank branches”.