What Happened to Nanotech?

Follow James on Twitter @jwangARK

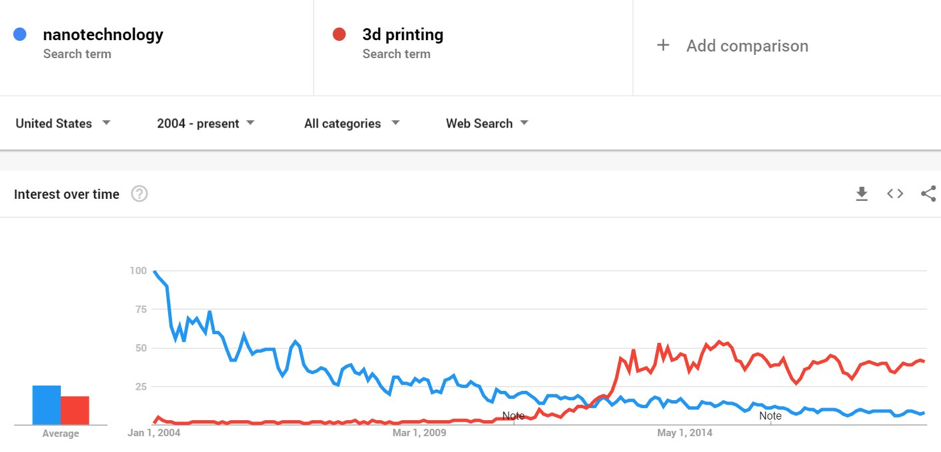

Bill Joy’s famous 2000 essay, Why The Future Doesn’t Need Us, named three technologies set to transform the 21st century: robotics, genomics, and nanotech. Almost two decades later, robotics and genomics have made great strides, but nanotech seems to have faded away. Google Trends offers some perspective—the number of searches for “nanotechnology” has fallen by more than 90% since 2004, as shown below.

Source: Google Trends

Nanotech—specifically molecular nanotechnology--is seldom mentioned these days because researchers haven’t found a way to make it work. The original vision called for tiny nanoscale robots that could manipulate matter at the molecular level, enabling them to build anything imaginable. The challenge was building a robot small and dexterous enough to transport individual molecules. Joy expected a solution by 2020 but, thus far, no breakthrough has overcome the obstacles.

In the absence of a nanotech revolution, 3D printing is enjoying a revival. Like nanotech, 3D printing creates objects from the bottom up, but at a larger scale. Unlike nanotech, 3D printing works. Today it’s printing shoes, hearing aids, rocket engines, and even satellites.

ARK estimates that 3D printing revenues could scale more than 10-fold during the next five years, from less than $10 billion today to $94 billion in 2023.

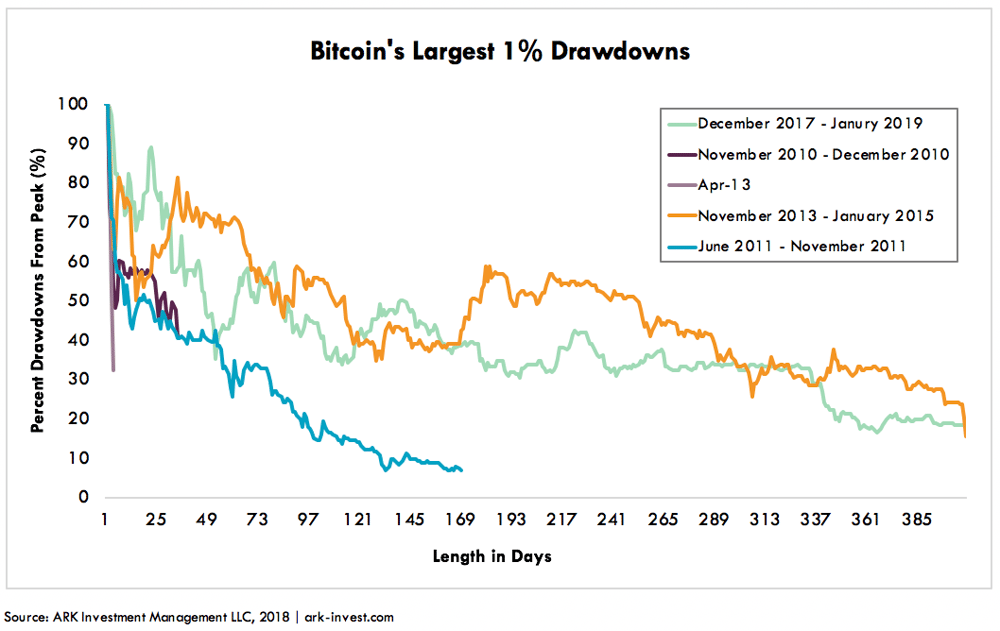

Bitcoin’s Price Drawdowns in the Last Ten Years Hold Some Clues to Its Recovery

Follow Yassine on Twitter @yassineARK

Bitcoin's recent price drop from roughly $20,000 at its peak in 2017 to $3,200 is neither its longest nor its most severe drawdown. The charts below show bitcoin’s recent price drop in the context of historical drawdowns:

Thus far the bitcoin price has suffered an 85% drawdown over 380 days, assuming that $3,200 was its trough. During 169 days in 2011, it dropped 93%, and over 407 days in 2013-15, 86%.

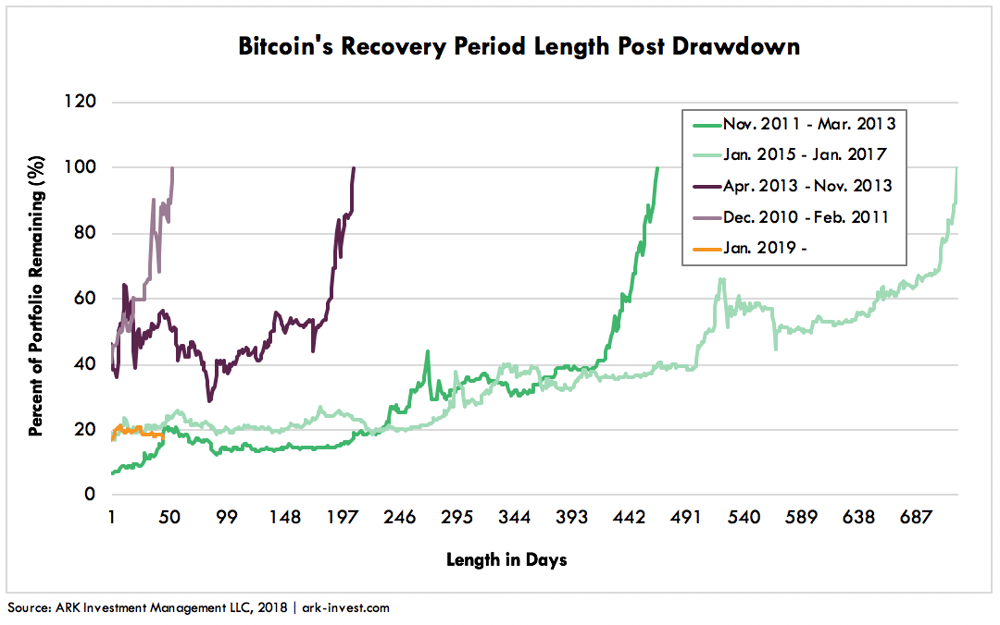

For the most part, bitcoin’s recovery from trough to previous peak has taken longer than the period from peak to trough, as shown below:

The 93% drawdown in 2011 took approximately 1.5 years to recover, and the 86% drawdown from 2013-15, nearly 2 years. Today, if $3,200 was the trough in late 2018, then bitcoin has been in recovery for just 40 days. That said, even if the recovery in bitcoin back to $20,000 were to take 3-5 years this time around, the 6-7 fold increase probably would outstrip the returns from any other asset class.