According to TSMC, Moore’s Law Is Not Dead… It’s Not Even Dying

Follow James on Twitter @jwangARK

TSMC—the world’s leading chip foundry—does not believe in the death of Moore’s Law. Its Vice President of Research, Philip Wong, says that Moore’s Law is chugging along and should power TSMC for the next three decades.

TSMC is leading the industry with 7nm chip manufacturing, enabling customers like Apple and AMD with power efficient processors. The next node, 5nm, already is in risk production, and 3nm already is in early development. As they approach the size of atoms, however, transistors will require novel manufacturing techniques to reach higher density and performance.

The main path forward appears to be3D integration—stacking chips on top of one another. Already in use for high performance memory today, TSMC believes that stacking memory and logic will improve memory capacity and bandwidth, both critical for AI applications. With next generation nanomaterials, memory performance could improve almost 2,000-fold.

We believe that despite TSMC’s upbeat messaging, Moore’s Law during the next few decades is unlikely to resemble the past. Innovation is moving from transistors to packaging technology, making chip architecture and software optimization even more important going forward.

Unlike in the PC era when Intel’s x86 architecture dominated, AI probably will require more heterogenous architectures, with many designs for many markets. TSMC, we believe, is the agnostic enabler in such a world. Unless Intel is able to win on multiple fronts - CPUs, GPUs, AI accelerators, and automotive - it probably would be better off parting with its fabs.

Here Is Our Preamble to What We Believe Has Gone Wrong With Venture Capital

Follow Max on Twitter @mfriedrichARK

In the process of writing a white paper detailing the overvaluation and excesses in the pre-IPO venture capital space, we have come across several data points that we would like to share.

The venture capital industry been the beneficiary of a “gold rush” during the past decade. Pension funds alone have increased their allocation to alternative assets, including venture capital, from 7% in 2008 to 20% in 2017, a $2 trillion shift. In addition, between 2014 and 2018 large university endowments nearly doubled their exposure to venture capital, following David Swensen’s 20-year lead at Yale. In return, in 2018 alone venture capitalists deployed a record $258 billion into startups globally. As a result, during the past five years, the number of startups valued at more than $1 billion - so-called unicorns - has jumped five-fold from 80 to more than 400, with an unrealized value of $1.7 trillion waiting to tap the public markets.

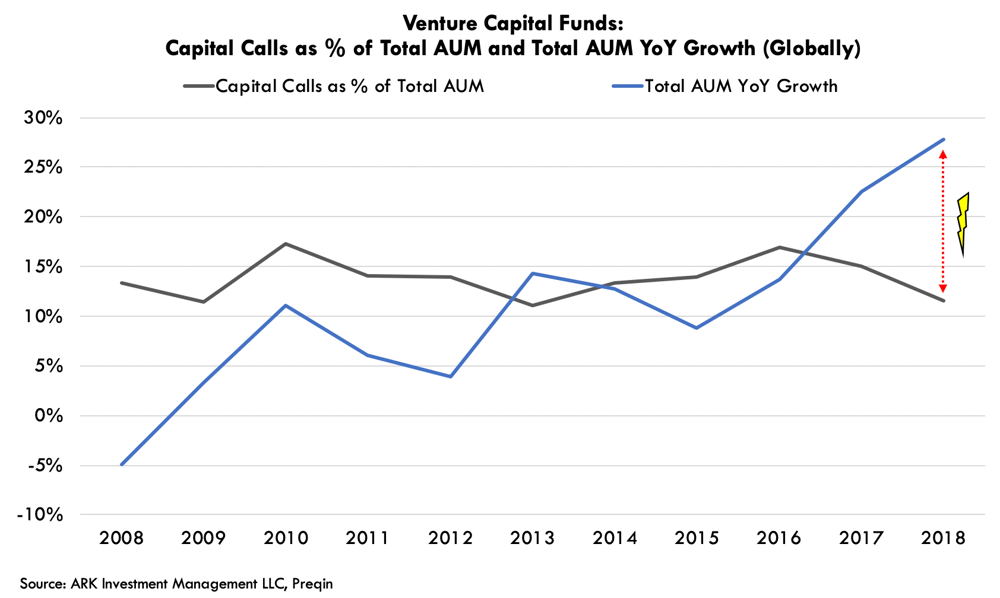

While venture capital has enjoyed a period “up and to the right,” this week Preqin released fund data that calls into question the sustainability of that trend. Since 2016, for example, venture capital assets under management (AUM) have been growing rapidly while their capital calls as a percentage of AUM have been declining, as shown below. In dollar volume during 2018, capital calls declined 2% on a year over year basis while AUM grew 28%, suggesting that the demand for venture capital is lagging behind the supply, inflating valuations. As a result, startups are buying $60 million private jets and opening restaurants as the discipline associated with traditionally tight funding disappears. Increasingly, we believe the revenue growth of VC-funded startups is a function more of fundraising than of business strategy, with negative gross margins the result.

Many VCs continue to fund their startups without regard to fundamentals because higher valuations and paper returns enable follow-on funds and increased management fees. As a result, the odds that other investors, particularly in the public markets, will pay a premium for these startups are declining, leaving VCs increasingly with dry powder unable to generate returns. At some point, the limited partners (LPs) are sure to take notice and turn off the taps, pushing valuations back into line.

Why Are Brokerage Companies Slashing Fees for US Trades?

Follow George on Twitter @GeorgeOfARK

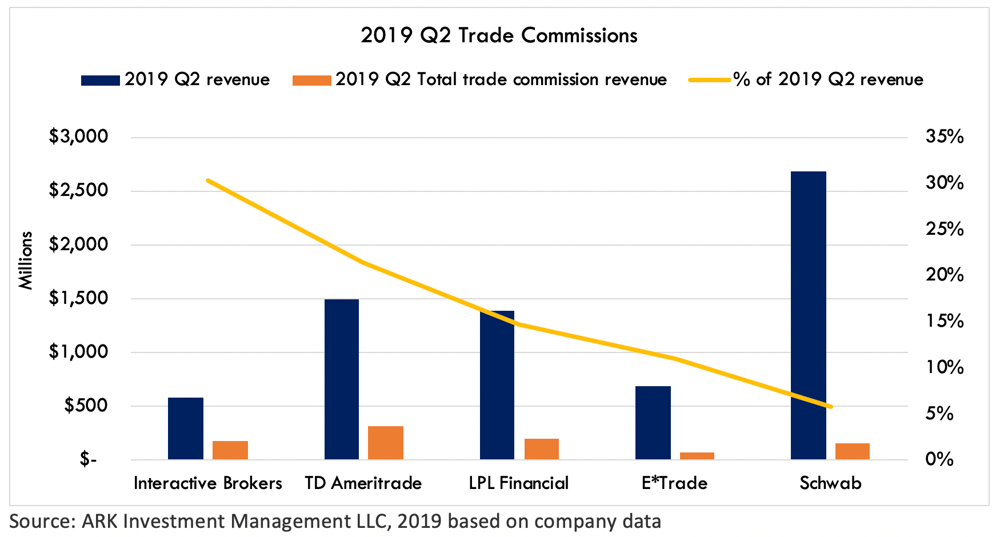

Last week, Interactive Brokers introduced a new service called IBKR Lite, eliminating fees on US equity, ETF and option trades. Charles Schwab followed on October 1st, as did TD Ameritrade, E*Trade and LPL Financial soon thereafter. All of their stocks suffered, TD Ameritrade (AMTD) - down 26% - faring the worst. During the second quarter, TD Ameritrade made $320 million from commissions, representing ~22% of total revenues, as shown below. (Note, IBKR Lite is not a part of Interactive Brokers’ base business, suggesting that its zero-fee structure will not have the disproportionate impact suggested by the chart below.)

Founded in 2013, Robinhood has been a disruptive force in the retail brokerage industry. With an estimated 6 million users today, it has raised ~$900 million in venture capital funding to date and shows no signs of slowing down thanks in large part to its low customer acquisition costs. Reportedly, Square also is introducing stock trading to its Cash App, adding yet another competitive threat to the incumbents.

While Robinhood offers free stock trading, its revenue base is buttressed by fees from securities lending and selling order flow to high frequency traders. In 2018 Bloomberg reported that Robinhood made ~40% of its revenue from selling its order flow, a controversial practice highlighted in Michael Lewis’s Flashboys. Schwab also provides some of the same ‘execution services’. As zero-fee commissions boost order flows, selling them to high frequency traders could offset some of the lost commissions in this increasingly disrupted part of the financial markets.

Did the SEC Let EOS Off the Hook?

Follow Yassine on Twitter @yassineARK

In June, the SEC announced it was suing Kik for conducting an Initial Coin Offering (ICO) of its Kin token in 2017. This week, the crackdown continued, as the SEC announced a settlement with Block.one, the company behind the EOS blockchain.

The SEC alleges that EOS’s ICO was in violation of the Securities Act of 1933, as it did not register the sale of its $4.1 billion offering. Block.one has agreed to a $24 million-dollar penalty, equivalent to 0.6% of total capital raised.

Since the announcement, the community has criticized the SEC heavily. In the past, the SEC insisted that the sale of securities must play by SEC rules or suffer the consequences. Yet, the discrepancy between funds raised and the penalty seems to indicate that not “playing by the rules” makes more sense for entities issuing ICOs.

As The Block’s Larry Cermak notes, the recent Blockstack offering is a case in point. “Blockstack completed the first SEC-approved token offering, raising $23 million. But Blockstack spent 10 months and $2 million getting SEC approval for the Reg A+ sale. That’s 8.7% of the total raise in contrast to 0.6% that Block.one had to pay to the SEC.”

The question is whether or not Block.one’s settlement with the SEC establishes precedent. Because it was not the result of a lawsuit but instead an administrative settlement, the answer is not clear.