It's Monday, February 24th, 2020. Please enjoy ARK's weekly newsletter curated by our thematic analysts and designed to keep you engaged with disruptive innovation. Have a wonderful day!

A New Ridehailing Company May Turn Uber And Lyft Into Sitting Ducks

ARK hypothesized1 that once fully autonomous cars commercialize, Uber and Lyft will lose the 20-30% platform fees they take today. Indeed, they will be lucky to get 1-5% in lead generation fees as they are forced to partner with autonomous technology providers.

Not only in the long term but perhaps in the short term as well, autonomous technology companies seem well positioned to capture the lion’s share of the economics from Uber, Lyft, and other ridehailing companies. On its recent earnings call, Tesla reiterated that it plans to launch a ride hailing service with drivers as early as this year, before solving for full autonomy. If so, it will learn how to operate a ridehailing network and will collect much more data to train its Autopilot system in preparation for the launch of its fully autonomous taxi network. As it competes with Uber and Lyft, Tesla also will generate recurring cash flow from a new revenue line item on its income statement, mitigating the need to go back to the capital markets as it scales manufacturing capacity globally.

A Model 3 is likely to provide ridehailing drivers with superior economics compared to the widely used Toyota Camry. According to ARK’s analysis, thanks to lower maintenance and fuel costs, the Model 3’s cost per mile driven will be roughly one third lower than that of the Camry. Not included in this analysis are insurance costs: Tesla probably will self-insure, offering lower rates for drivers activating Autopilot on a regular basis. Based on all of these lower costs, not only should drivers on the Tesla Network take home more pay than with Uber, but Tesla also may enjoy a higher take rate than Uber’s 23% average today. This potential win-win could become a triple win perhaps as ridehailing customers choose what we believe is the more appealing car. In fact, Tesla might be able to charge UberBlack rates on the Tesla Network as it adds a recurring revenue stream to each Model 3 sold.

The value proposition of Tesla’s ridehailing network is likely to hit Uber and Lyft hard. Competition in the ridehailing market is already fierce, and Tesla is about to turn up the heat!

[1] Please refer to pages 40 – 45 of ARK’s Big Ideas 2020

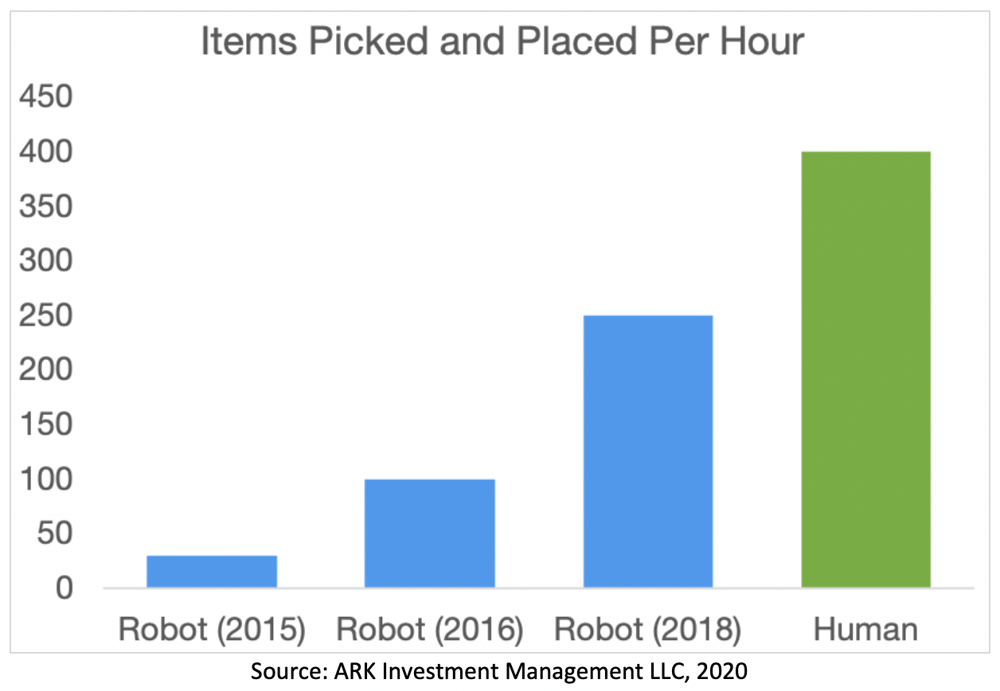

2020 Could Be the Year That Robots Pick and Place at the Same Rate as Humans

Amazon held its first robot pick and place challenge in 2015. As shown below, that year the winning team picked and placed the equivalent of 30 items per hour, paling in comparison to the human average of 400 items. Then, in the three years ended 2018, robot picking and placing improved more than eight-fold to 250 items per hour, as shown below.

This year, German electrical supplier Obeta reportedly introduced robots that outperform humans, thanks to AI robotics company Covariant. Though not completely comparable to items picked and placed per robot per hour, Obeta claims that a Covariant-powered robot can fill more than 200 orders per hour, surpassing the 170 average of humans. Perhaps most impressive is the AI system’s learning rate. After training for five months, the percent of Obeta’s products that the robots picked successfully improved from just 15% to roughly 95%.

A Clever Flash Loan Has Exploited “DeFi” Protocol bZx

bZx, a decentralized finance (DeFi) protocol for tokenized margin trading and lending, was exploited by a flash loan. A flash loan allows an individual to borrow capital without collateral, as long as he returns it in a single transaction. In other words, in seconds users can tap significant capital and carry out an attack at no cost. While not the enablers of the attack, flash loans have raised questions about the DeFi’s sustainability.

Attacker takes advantage of the dYdX flash loan feature to borrow 10,000 ETH.

Attacker deposits 5500 ETH into Compound as collateral to borrow 112 WBTC.

Attacker deposits 1300 ETH into bZx to take advantage of the margin trade feature and to short ETH in favor of WBTC. bZx calls KyberSwap to swap the borrowed ETH for WBTC in return. Consulting reserves, Kyberswap finds the best rate for swap on Uniswap, artificially driving WBTC price up on Uniswap.

With inflated WBTC price, attacker sells 112 WBTC borrowed from Compound for WETH in Uniswap, netting ETH in return.

With the ETH, attacker repays the flash loan to dYdX, pocketing the remaining ETH.

As Block journalist Celia Wan notes, “The recentattacks on DeFi lending protocol bZx, enabled by flash loans, serve as a wake-up call to other DeFi projects that may have been underestimating their adversaries.”

‘UNCALLED’ Enhances the Power of Nanopore Sequencing Instruments

Oxford Nanopore Technologies (“ONT”) recently announced several hardware and software upgrades that ARK believes will make its sequencers more attractive to clinical diagnostic providers. Previously, diagnostics companies shunned ONT instruments because of their inferior accuracy, frequent update requirements, and lower sample throughput. We summarized several of its improvements in a recent newsletter. Now, two academic groups have published papers highlighting the benefits of ONT’s system upgrades and the advantages of sequencing with nanopore technology.

In clinical settings, typically diagnosticians prepare DNA samples by making many copies of genetic regions of interest prior to sequencing, the most expensive part of the DNA sequencing process. The chemicals used in this step can cause errors or destroy portions of the genetic material. One academic group built UNCALLED, an open-source software tool that eliminates the need to pre-select regions of interest using chemicals. UNCALLED takes advantage of ONT’s ‘read-until’ API, allowing researchers to enter digitally the parts of the genome in which they are interested. As shown in this chart, a nanopore will sequence DNA completely only if it matches the region specified by the researcher or diagnostician. UNCALLED should allow for lower sample prep costs while preserving the fidelity of DNA samples.

While this improvement increases the likelihood of clinical adoption, ONT has had a history of over-promising and under-delivering on an “Illumina-killer” for roughly a decade. If successful in any way, however, ONT will introduce more competition into the sequencing space, perhaps giving Illumina (ILMN) an incentive to accelerate its own cost declines and maintain its competitive advantage.

In Other Innovation News

Facebook’s New Pinterest-Killer App Disappoints

Facebook hopes that its new lifestyle app Hobbi will dethrone Pinterest, but a rocky first week on the App Store suggests otherwise. Hobbi has a 2-star out of 5-star rating, suggesting poor user satisfaction. One user explained, “Basically [it’s] just a bad version of Pinterest. Might as well just use that instead”. Copying Pinterest isn’t the surprise, as it is Facebook’s modus operandi nowadays. We are wondering, however, why Facebook would spin out a new app instead of integrating Pinterest-like features into Instagram. Maybe Hobbi is just a hobby for Facebook.

Cash App Goes Viral on Tik Tok

Largely unnoticed by investors, Square’s Cash App has gone viral on TikTok during the last two months. Launched with a sponsored post on Genius in December, Cash App payed TikTok influencers to record videos including its Cash App song and post the content with hashtag #cashappthatmoney. The videos have attracted more than 140 million Tik Tok views to date. We believe that Cash App’s network-based marketing strategy has been critical to its growth. Please see this Twitter thread for our detailed explanation.

LendingClub Acquires Radius Bank, Potentially Adding Significantly to Its Profitability

On Tuesday LendingClub announced that it is acquiring Radius Bank for $185 million. While Lending Club previously had announced its intention to apply for a bank charter, this acquisition should accelerate the process. A bank charter should lower its origination and funding costs, providing savings of roughly ~$80 million and, all other things equal, could increaseprojected 2020 net income by 216%. A bank charter also should allow LendingClub to offer new products such as checking accounts and debit cards to its existing customer base.

ARK's statements are not an endorsement of any company or a recommendation to buy, sell or hold any security. For a list of all purchases and sales made by ARK for client accounts during the past year that could be considered by the SEC as recommendations, click here. It should not be assumed that recommendations made in the future will be profitable or will equal the performance of the securities in this list. For full disclosures, click here.

You received this email because you are subscribed to Research NewslettersfromARK Investment Management LLC. Unsubscribe from ARK emails or choose the types of emails you want to receive. Unsubscribe from all.

This Newsletter is for informational purposes only and does not constitute, either explicitly or implicitly, any provision of services or products by ARK Investment Management LLC (“ARK”). Investors should determine for themselves whether a particular service or product is suitable for their investment needs or should seek such professional advice for their particular situation. All content is original and has been researched and produced by ARK unless otherwise stated therein. No part of the content may be reproduced in any form, or referred to in any other publication, without the express written permission of ARK. All statements made regarding companies, securities or other financial information contained in the content or articles relating to ARK are strictly beliefs and points of view held by ARK and are not endorsements of any company or security or recommendations to buy or sell any security. By visiting and/or otherwise using the ARK website in any way, you indicate that you understand and accept the terms of use as set forth on the website and agree to be bound by them. If you do not agree to the terms of use of the website, please do no access the website or any pages thereof. Any descriptions of, references to, or links to other products, publications or services does not constitute an endorsement, authorization, sponsorship by or affiliation with ARK with respect to any linked site or its sponsor, unless expressly stated by ARK. Any such information, products or sites have not necessarily been reviewed by ARK and are provided or maintained by third parties over whom ARK exercises no control. ARK expressly disclaims any responsibility for the content, the accuracy of the information, and/or quality of products or services provided by or advertised on these third-party sites.

This year, German electrical supplier Obeta reportedly introduced robots that outperform humans, thanks to AI robotics company Covariant. Though not completely comparable to items picked and placed per robot per hour, Obeta claims that a Covariant-powered robot can fill more than 200 orders per hour, surpassing the

This year, German electrical supplier Obeta reportedly introduced robots that outperform humans, thanks to AI robotics company Covariant. Though not completely comparable to items picked and placed per robot per hour, Obeta claims that a Covariant-powered robot can fill more than 200 orders per hour, surpassing the