It's Monday, March 2nd, 2020. Please enjoy ARK's weekly newsletter curated by our thematic analysts and designed to keep you engaged with disruptive innovation. Have a wonderful day!

MercadoLibre Appears to Be Revolutionizing SME Lending with Alternative Data and Machine Learning

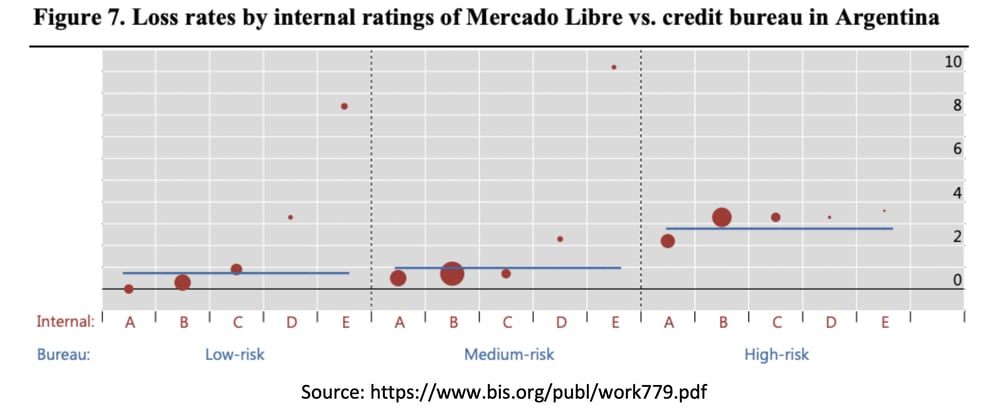

Using alternative data and machine learning, MercadoLibre seems to have gained a competitive advantage in identifying both high-risk borrowers and companies that otherwise would not qualify for credit. With data from more than 81,000 sellers in Argentina, MercadoLibre’s internal credit ratings contrasted significantly from those of traditional credit bureau ratings, based on research from the International Bank of Settlements (IBS) and illustrated in the chart below. The IBS graphed MercadoLibre’s loans based both on credit bureau ratings and on MercadoLibre’s A-E rating scale.

As illustrated by the blue line, the average loss rate on loans that credit bureaus would have categorized as “High-risk” was 2.8% which, according to the authors, is “similar to the premium [small or medium enterprise] SME segment at traditional banks”. In other words, with alternative data MercadoLibre identified companies at low risk of default that traditional credit bureaus would have rated negative. According to the authors, such “High-risk” borrowers make up 30% of MercadoLibre’s credit portfolio. Perhaps more interesting, MercadoLibre identified high-risk borrowers whom the credit bureau classified incorrectly as “Low-risk” or “Medium-risk”, as shown by the outliers in category “E” within the bureau’s “Low-risk” and “Medium-risk” ratings.

Waymo Is Ramping Headcount but Could Continue to Lag Behind Competition

This week, The Information reported that Waymo has increased its headcount from 800 to 1,500 during the past year. Now that Larry Page and Sergei Brin have ceded their leaderships roles, ARK has been wondering if Alphabet will look at Waymo with a more critical eye and perhaps consider a spinoff. News of increased headcount seems to suggest that Waymo is doubling down on its efforts to scale an autonomous taxi service.

Waymo has struggled to launch a commercial autonomous service in Phoenix, perhaps because of a data problem. Compared to its database of 20 million real world miles driven since inception, Tesla has the option to draw from more than 20 million miles of driving data in a single day thanks to its customer fleet of more than 700,000 Autopilot-enabled cars. Waymo’s prototype fleet might have more autonomous functionality than any other vehicles on public roads today, but without enough data to solve for full autonomy, it could be lapped by the competition.

For decades, startups have been funded almost exclusively by venture capital. As the startup ecosystem matures, however, debt could become a viable alternative for mid to late stage funding, argues Alex Danco.

While the debt market has ignored startups because of their unpredictable businesses and the lack of collateral, Software-as-a-Service (SaaS) companies are different. Individual SaaS customers may come and go but, as annual cohorts, their churn and cash generation profiles are fairly predictable. At the same time, the go-to-market strategy of SaaS companies typically relies heavily on sales and marketing which delivers recurring revenues. The upfront cash necessary to acquire predictable streams of future revenue is suitable to debt instead of equity financing. A SaaS startup should be able to issue a “2022 cohort customer collateralized bond” instead of raising equity to fuel growth for the next one or two years.

Whether debt will fund startup SaaS companies remains to be seen. If it does, late stage venture, already competing with Softbank and private equity, will face even greater pressures.

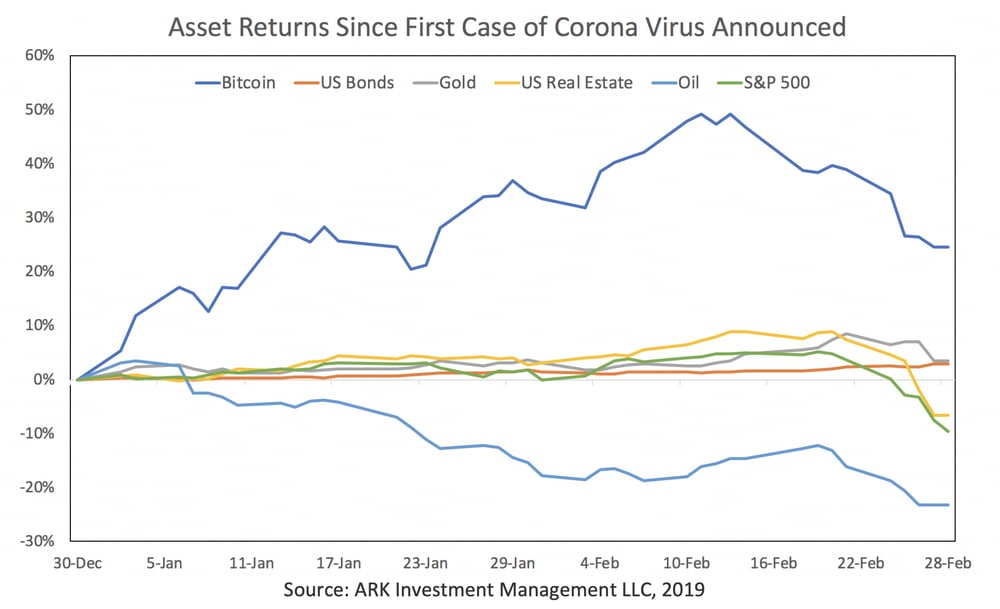

As fear about the coronavirus’s impact on the economy escalates, investors have been quick to assess bitcoin as a “digital gold, safe haven” asset.On January 30th, The World Health Organization (WHO) declared the coronavirus outbreak a global emergency after the number of cases had spiked by an order of magnitude and the death toll had increased to 213.

Since the WHO declaration, bitcoin’s (BTC’s) price has dropped 8.5% while price of gold has appreciated 1%. Many are wondering why the price of “digital gold” did not mirror that of physical gold. As Coinmetrics notes, “While market participants are quick to point out instances where BTC’s correlation with gold is high, such as during the summer in 2019, much less attention is paid to instances where BTC should react to safe haven capital flows but doesn’t.”

Assessing asset class returns on a slightly longer time horizon, however, paints a different picture. Since China reported the first case of coronavirus on December 30th, bitcoin has outperformed every major asset class, including gold. As shown below, bitcoin and gold have appreciated 23% and 4%, respectively, while the S&P 500 has dropped 9.5%. Over the longer-term time period, XBT’s appreciation seems to illustrate a lack of correlation to the returns of most traditional asset classes.

Is Illumina Facing Pricing Pressure from China’s Sequencing Instruments?

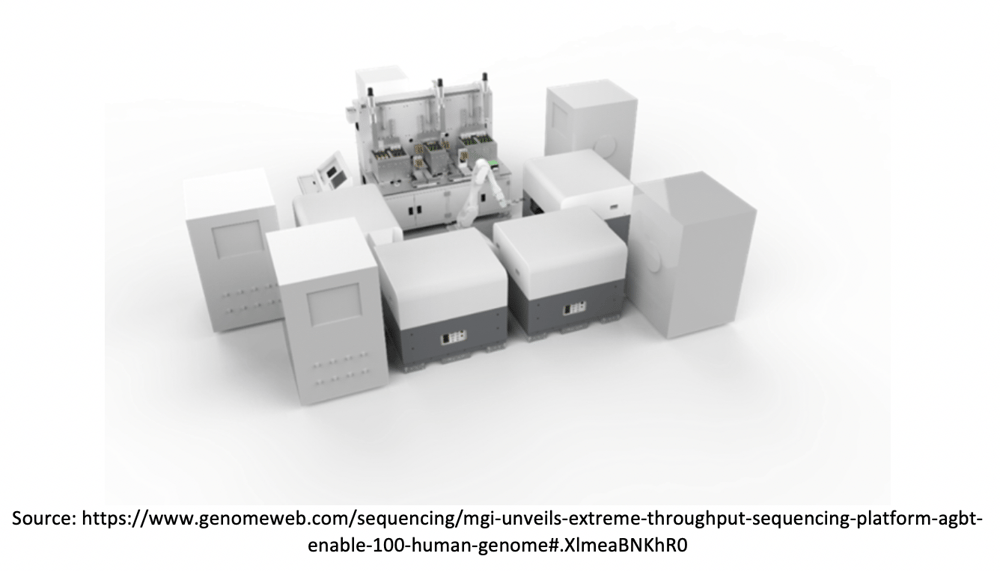

A subsidiary of China’s Beijing Genomics Institute (BGI), MGI recently unveiled an ‘extreme throughput’ sequencing platform ostensibly enabling a $100 human genome. In our view, Illumina opened itself up to this competitive incursion because its HiSeq X system, after enabling the $1,000 genome in 2014, has not dropped prices significantly in more than five years. ARK believes that Illumina has not cut prices because it has enjoyed an effective monopoly, until now perhaps.

While impressive technologically, MGI’s newest instrument, the DNBSeq Tx, seems too complicated and is unlikely to commercialize widely. Unlike Illumina’s self-contained sequencers, the Tx platform involves a large robotic workspace, as shown below. Like other sequencers, it achieves its lowest cost per genome only when running at full capacity. To hit the $100 genome, the Tx requires $70,000 - or 700 samples - to run the platform once, limiting adoption to high throughput customers such as large population sequencing sites.

Despite its commercialization challenge, the Tx system does contain novel advancements, importantly CoolMPS chemistry which will integrate backwards with the rest of MGI’s instrument portfolio. Once fully integrated, CoolMPS should enable higher accuracy and improved operating costs.

MGI’s second-highest throughput instrument, the T7, purports to sequence a genome for as little as $500 and could intensify competition in the United States later this year, unless Illumina’s patent infringement suit stops it. According to MGI, even at 25% capacity utilization, the T7 can sequence genomes for $500. Goaded by prospective competition, ARK believes that Illumina will upgrade the NovaSeq with super-resolution optics and its new two-color chemistry, aiming for a $100 genome and ultimately benefiting from the massive latent demand unlocked by lower sequencing costs.

In Other Innovation News

Wind Is the Leading Source of Renewables In The US

Electricity generated from wind power overtook hydropower and was the leading source of renewable electricity in 2019. Wind power produced 7.8% of total electricity last year, up from 1.9% in 2009. For additional perspective, the Energy Information Administration estimates that solar and wind will account for 76% of new generation installed this year.

Volkswagen’s EV Software Problems Could Cost More than $800 Million to Fix

Reports have surfaced suggesting that VW’s ID3 electric vehicle is plagued with software issues. ARK estimates that the cost to fix these bugs could top $800 million, roughly the cost to develop a new electric vehicle. One often cited paper estimates the cost at $10 per line of code. VW is on record saying that its new cars have around 100 million lines of code, including infotainment.[1] Is this problem unique to VW, or will most traditional automakers face similar problems as they transition to EVs?

ARK's statements are not an endorsement of any company or a recommendation to buy, sell or hold any security. For a list of all purchases and sales made by ARK for client accounts during the past year that could be considered by the SEC as recommendations, click here. It should not be assumed that recommendations made in the future will be profitable or will equal the performance of the securities in this list. For full disclosures, click here.

You received this email because you are subscribed to Research NewslettersfromARK Investment Management LLC. Unsubscribe from ARK emails or choose the types of emails you want to receive. Unsubscribe from all.

This Newsletter is for informational purposes only and does not constitute, either explicitly or implicitly, any provision of services or products by ARK Investment Management LLC (“ARK”). Investors should determine for themselves whether a particular service or product is suitable for their investment needs or should seek such professional advice for their particular situation. All content is original and has been researched and produced by ARK unless otherwise stated therein. No part of the content may be reproduced in any form, or referred to in any other publication, without the express written permission of ARK. All statements made regarding companies, securities or other financial information contained in the content or articles relating to ARK are strictly beliefs and points of view held by ARK and are not endorsements of any company or security or recommendations to buy or sell any security. By visiting and/or otherwise using the ARK website in any way, you indicate that you understand and accept the terms of use as set forth on the website and agree to be bound by them. If you do not agree to the terms of use of the website, please do no access the website or any pages thereof. Any descriptions of, references to, or links to other products, publications or services does not constitute an endorsement, authorization, sponsorship by or affiliation with ARK with respect to any linked site or its sponsor, unless expressly stated by ARK. Any such information, products or sites have not necessarily been reviewed by ARK and are provided or maintained by third parties over whom ARK exercises no control. ARK expressly disclaims any responsibility for the content, the accuracy of the information, and/or quality of products or services provided by or advertised on these third-party sites.