It's Monday, April 27th, 2020. Please enjoy ARK's weekly newsletter curated by our thematic analysts and designed to keep you engaged with disruptive innovation.

Will People Stop Buying EVs Now That Gas Prices Are So Low?

While investors are asking if electric vehicle (EV) sales will fall now that gas prices have dropped so dramatically, ARK believes that the question misses the mark. It assumes that auto buyers make their decisions based on the total cost of ownership (TCO) which, if true, would suggest that EV sales should be much higher than they are today.

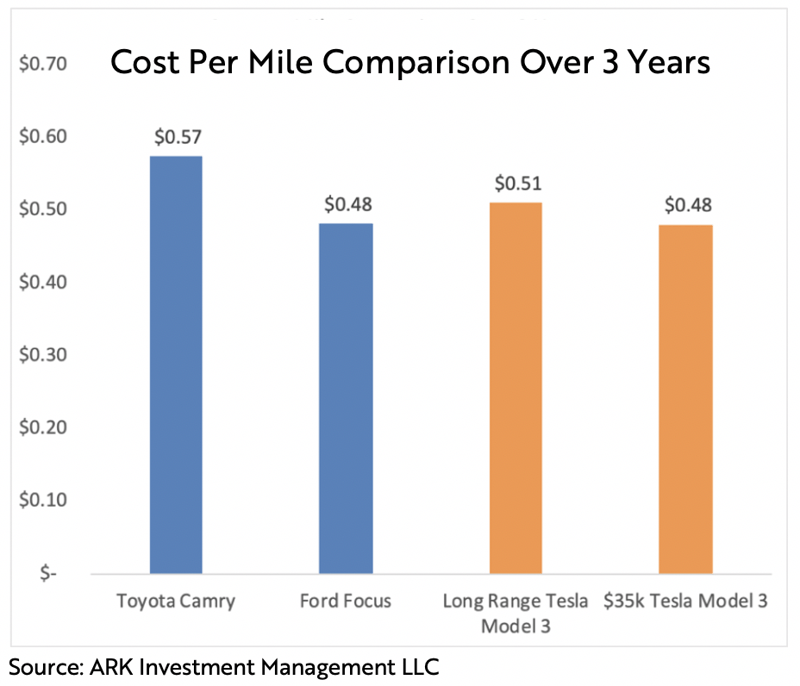

According to ARK’s research, over a three-year period the Long-Range Tesla Model 3 is already less expensive to own than a Toyota Camry, and the low-end Model 3 less expensive than a Ford Focus, as shown below. The TCO is much more sensitive to a vehicle’s residual value than to gas prices. In our view, the right question is how low the prices of used gas-powered cars will go as the market transitions first to electric vehicles, and then to autonomous electric vehicles.

ARK’s Takeaways From A Recent Talk By Tesla’s Andrej Karpathy

Recently, Andrej Karpathy, Head of Artificial Intelligence (AI) on Tesla’s Autopilot Team, offered several interesting insights on how Autopilot works in a video. First, he detailed how Tesla trains Autopilot with its customer-collected data feed using long tail examples like stop signs painted on buildings or those occluded by tree branches. To improve Autopilot’s reaction to these “corner cases”, Tesla sends a software detector to its 800,000+ vehicle fleet to identify images of, say, occluded stop signs. In contrast, with fleets of hundreds instead of hundreds of thousands driving in several cities instead of nationwide, GM’s Cruise Automation and Waymo have limited access to data on corner cases in training their vehicles.

Karpathy also explained how Tesla is bridging the gap between cameras and LiDAR. We previously heard about an Autopilot update involving 3D video labeling as opposed to 2D image labeling, enabling faster, more accurate image detection and path planning - Tesla’s solution to the LiDAR gap. LiDAR recognizes images and assesses direct depth more accurately than do cameras. In a two-step indirect process, cameras take shots of images and software gauges depth by analyzing the pixels. Mistakes involving a few pixels can translate into meters or yards of inaccuracy. By labeling 3D videos of driving scenes, Tesla is compensating for the camera’s weakness as the primary image sensor in its vehicles.

Karpathy also discussed Tesla’s local mapping which includes much less detail than the high definition maps its competitors use. While a Waymo vehicle drives with preloaded information about the exact location of a stop sign, within centimeters of accuracy, a Tesla would detect only the presence of a stop sign somewhere in the vicinity. In addition to vague local maps and its camera-based approach, 3D video labeling separates Tesla from its competitors, enabling the recognition of corner cases in solving for full autonomy.

We believe Tesla’s approach is highly differentiated and will be almost impossible for a competitor to replicate. While autonomous driving is an extremely complex problem to solve, Tesla could enjoy a near-monopoly in autonomous ride hailing if it is successful.

COVID-19 Related Delays in Clinical Trials Could Expose How Inflated Estimates of Development Costs Are

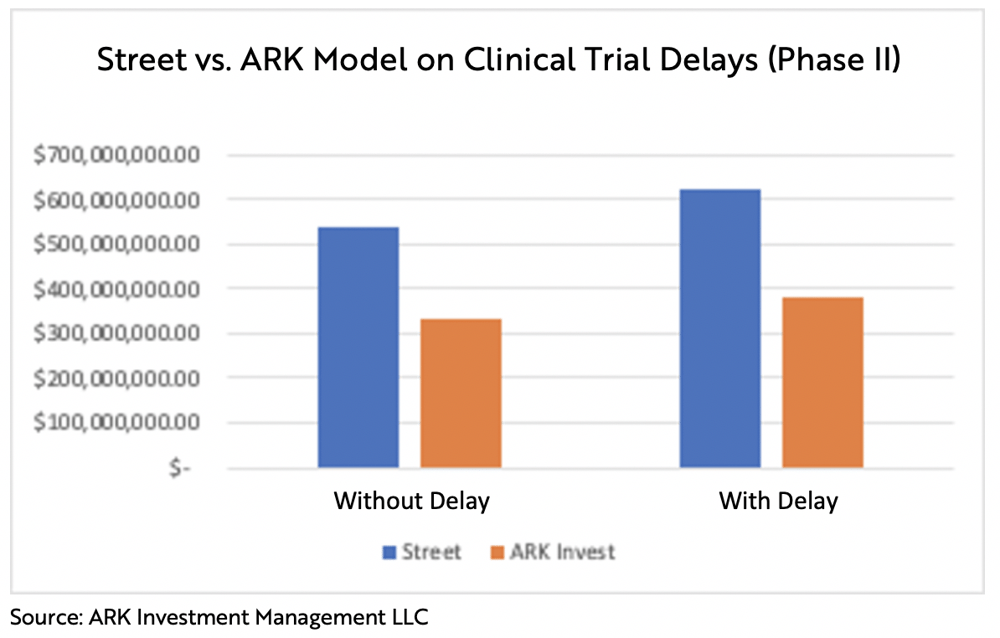

The drug development process is arduous and expensive. Sell-side, or Street, analysts estimate that the total cost of drug development is approximately $540 million per drug on average,1 a gross overestimation in ARK ‘s view.

On average, the Street estimates that a one-year delay in a Phase II trial would increase the cost of drug development from $540 million to $625 million.1 Street models, however, do not account for the improvements in R&D efficiency that the convergence of three technologies - sequencing, artificial intelligence (AI), and gene editing - is delivering. That convergence is reducing time-to-market and lowering the failure rate of drug candidates. We are modeling improvements of 10% and 25%, respectively,1 in the drug failure rate and time-to-market. As a result, ARK’s forecast of the average clinical trial cost is below that of the Street’s, even after including the costs of a delay, as shown below.

COVID-19 seems to be delaying some clinical trials significantly, setting back research and development (R&D) budgets accordingly. Because we believe analysts’ R&D forecasts already were too high and now will move higher, innovative drug companies could be on the cusp of delivering upside earnings surprises.

Facebook’s Libra unveiled a host of changes to its proposed stablecoin. Initially slated to launch last quarter, the stablecoin was supposed to be backed by a basket of fiat currencies and government bonds. Notably, the Libra Association - an independent membership organization facilitating its operation and overseeing the administration of Libra reserves - would have had full discretion in deciding the composition of the basket. Upon the release of the first version of the white paper in June 2019, Facebook’s Libra faced an immediate backlash from regulators who refused to let Facebook threaten the monetary sovereignty of governments.

In an attempt to appease regulators, Facebook has announced significant revisions to the project. It included four key changes to its white paper.

It will offer single-currency stable coins in addition to the multi-currency coin.

A robust compliance framework will enhance the safety of the Libra payment system.

It will not transition to a permissionless system like Bitcoin’s.

The design of the Libra Reserve will include strong protections.

The changes mark significant concessions to regulators’ concerns. The Libra Association emphasized that the Libra network will complement fiat currencies, not compete with them. Furthermore, Libra wants to cater to central banks by serving potentially as a platform for central bank digital currencies.

Libra’s vision since initial inception has changed dramatically. Libra seems to be evolving into a compliant payment processor seeking to accommodate central banks instead of an open, global money seeking to bank the unbanked.

Facebook Bets Big on India with $5.7 Billion Investment in Jio

Facebook is investing $5.7 billion in Jio Platforms, India’s largest mobile internet carrier. Its largest investment in recent years, this deal signals Facebook’s ambition to capture India’s fledging $60 billion e-commerce market.

Saturated in most developed markets and blocked from China, Facebook is looking to India for growth. With approximately 400 million users, India is Facebook’s largest market by reach. Despite its size, India’s advertising market is fledgling and anemic, suggesting that Jio would be difficult to monetize with Facebook’s existing business model.

As a result, Facebook aims to capture India’s bourgeoning e-commerce market by combining Jio’s connection to the country’s 30 million small businesses with Facebook’s user network. Jio’s e-commerce platform could be integrated with WhatsApp to create Chinese style “super-apps” offering a variety of products and services, including digital payments and local delivery.

Facebook’s previous efforts in India – Free Basics and WhatsApp payments - have run into regulatory roadblocks. If nothing else, its alliance with Jio could help Facebook curry favor with the local governments and, thereby, the regulators.

Square is Starting to Integrate Its Consumer and Merchant Ecosystems

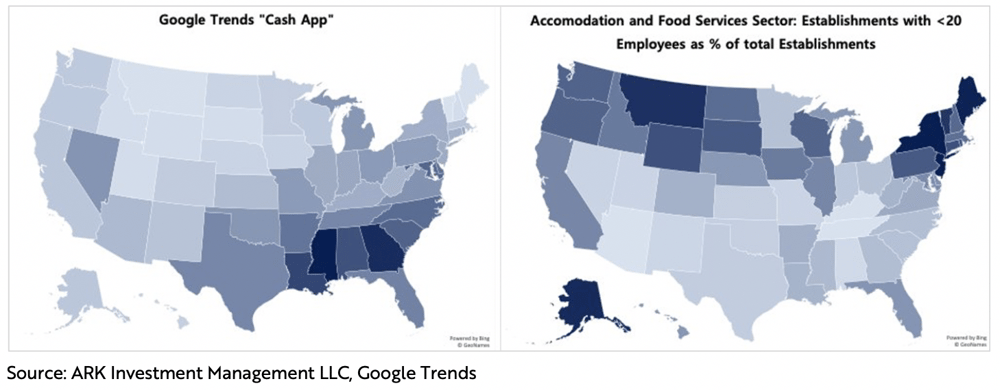

Cash App could become part of Square’s loyalty offering to merchants, according to a Square customer photo on Twitter. Because their geographic footprints share little overlap, Cash App and Square’s Point-of-Sale (POS) could leverage the new feature to acquire new users in both ecosystems.

In the US, Cash App’s users seem to be concentrated in the south, as shown in the chart on the left below, while Square’s POS concentration likely is elsewhere. POS probably has gained traction in regions more densely populated with independent coffee shops and other small to medium sized businesses, as shown in the chart on the right below. As a comparison of the two charts illustrates, independent small business penetration is high where Cash App penetration is low.1

In geographies with high Square POS and low Cash App penetration, the loyalty program could incentivize Square POS merchants and shoppers to download and use Cash App. Conversely, in regions with low Square POS but high Cash App penetration, Square could use the Cash App-based loyalty program as leverage to incentivize businesses to adopt Square’s POS. The latter could be the bigger beneficiary of this strategy in the short term, as Square’s Gross Payment Volume represents roughly 2% of total US card volume, while the percent of adults using Cash App at least once per month is more than 10%. Combined with Cash App’s Boost reward program, loyalty could become a revolutionary marketing platform for SMBs to reach local consumers.

[1] Explanation for right chart: Establishments ≠ firms. Firms consist of one or more establishments (e.g. chain locations). Square primarily sells to SMBs (using <20 employees as threshold in the Accommodation and Food Services sector). Square penetration should be high in states where the share of <20 employee establishments (e.g. independent coffee shops, bakeries etc.) is high. The sector “Accommodation and Food Services” includes coffee shops and was chosen as an example.

In Other Innovation News

‘Fortnite x Travis Scott’ Breaks Records

Astronomical, Travis Scott’s Fortnite debut, attracted more than 12.3 million concurrent players on Thursday night. Including those who watched via live streaming services like Twitch, more than 15 million people viewed Astronomical -- roughly a million more than the average viewership of the 2019 World Series. It also broke Fortnite’s last in-game attendance, DJ Marshmello’s concert, which attracted 10.7 million concurrent players, as shown in the chart below.

By hosting crossover events, Fortnite is becoming more than a game. Players are hanging out in its digital world and enjoying concerts like Astronomical, TV shows from Quibi, and even exclusive Star Wars movie trailers.

We hope you find this information useful and please stay safe.

ARK's statements are not an endorsement of any company or a recommendation to buy, sell or hold any security. For a list of all purchases and sales made by ARK for client accounts during the past year that could be considered by the SEC as recommendations, click here. It should not be assumed that recommendations made in the future will be profitable or will equal the performance of the securities in this list. For full disclosures, click here.

You received this email because you are subscribed to Research NewslettersfromARK Investment Management LLC. Unsubscribe from ARK emails or choose the types of emails you want to receive. Unsubscribe from all.

This Newsletter is for informational purposes only and does not constitute, either explicitly or implicitly, any provision of services or products by ARK Investment Management LLC (“ARK”). Investors should determine for themselves whether a particular service or product is suitable for their investment needs or should seek such professional advice for their particular situation. All content is original and has been researched and produced by ARK unless otherwise stated therein. No part of the content may be reproduced in any form, or referred to in any other publication, without the express written permission of ARK. All statements made regarding companies, securities or other financial information contained in the content or articles relating to ARK are strictly beliefs and points of view held by ARK and are not endorsements of any company or security or recommendations to buy or sell any security. By visiting and/or otherwise using the ARK website in any way, you indicate that you understand and accept the terms of use as set forth on the website and agree to be bound by them. If you do not agree to the terms of use of the website, please do no access the website or any pages thereof. Any descriptions of, references to, or links to other products, publications or services does not constitute an endorsement, authorization, sponsorship by or affiliation with ARK with respect to any linked site or its sponsor, unless expressly stated by ARK. Any such information, products or sites have not necessarily been reviewed by ARK and are provided or maintained by third parties over whom ARK exercises no control. ARK expressly disclaims any responsibility for the content, the accuracy of the information, and/or quality of products or services provided by or advertised on these third-party sites.