It's Monday, May 11th, 2020. Please enjoy ARK's weekly newsletter curated by our thematic analysts and designed to keep you engaged with disruptive innovation.

“How Many Gigafactories Will Tesla Build?”...is the Wrong Question

Investors often wonder how many gigafactories Tesla will have to build to sustain or increase its 17% global EV market share and meet our expectations. In our view, this question assumes that Tesla faces several constraints on its ability to scale, assumptions with which we disagree.

What are those constraints?

Battery production

Management bandwidth

Vehicle painting

Each of these “constraints” is likely to fall away during the next few months. At Battery Day in May or June, we believe Elon Musk probably will describe how Tesla will scale to terawatt-hour levels of capacity, eliminating the first constraint.

Meanwhile, we believe concerns about the constraints associated with management bandwidth and vehicle painting could diminish significantly as Tesla announces its plans for capacity per factory and for ‘cyber’ electric vehicles. Instead of building factories in different locations, Tesla is likely to expand the footprints of existing factories, eliminating the painting-related bottlenecks with a shift in production to ‘cyber’ vehicles. Painting vehicles causes two bottlenecks, production and emissions, explaining why the largest auto factory in the world manufactures only one million vehicles per year. Tesla’s stainless steel ‘cyber’ EV will obviate the need for paint, making it an ideal candidate to proliferate on an autonomous ridesharing platform. Not only resistant to scratches and dents, the ‘cyber’ EV also could scale to millions of units produced in a single factory.

In ARK’s view, the right question is, “How big will each of Tesla’s factories be?”

Lime’s Downround Confirms That Scooters Make for an Unattractive Business

This week we learned that, Lime’s latest funding round was at a $510 million valuation, less than a quarter of the $2.4 billion in its last round. More than a coincidence, Uber led the round and is combining its scooter and bikeshare business, Jump, with Lime.

ARK’s research suggests that scooter sharing is not a profitable business today and will deteriorate further in the next few years when autonomous taxis are likely to commercialize. As a result, Lime’s downround in valuation is not surprising, nor is Uber’s decision to off load Jump as it aims for profitability. ARK expects more shakeups in the mobility space as autonomous electric driving forces a consolidation in the auto industry, with COVID-19 only accelerating the process.

Could Cell Therapies Gain Market Share in Treating Solid Tumors?

Although approved only for liquid tumors today, ARK believes that cell therapies will treat solid tumors as well in the future. In our view, cell therapies are poised to capture share from “one size fits all” cytotoxic chemotherapies, with CAR-T therapies enjoying an annual revenue opportunity of more than $400 billion. Early-stage solid tumor treatment is likely to be the largest value driver.

Given the trajectory of legacy immunotherapies, cell therapies probably will become first line treatments roughly four years after their approval as second line treatments. Tumor Infiltrating Lymphocytes (TILs) are potent cell therapies rapidly gaining traction in solid tumors. TILs amplify the host immune system and, with a highly personalized one-time treatment, aim to cure the cancer.

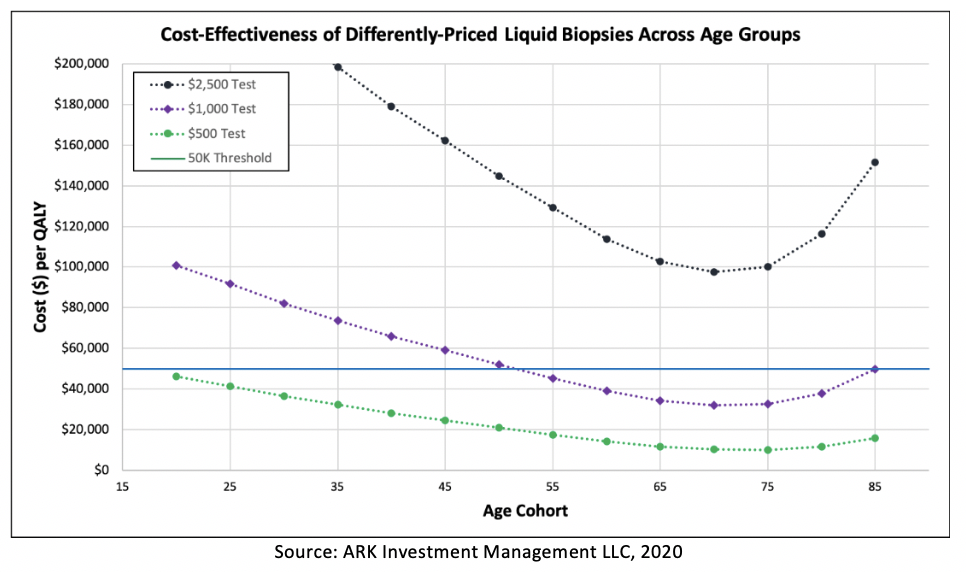

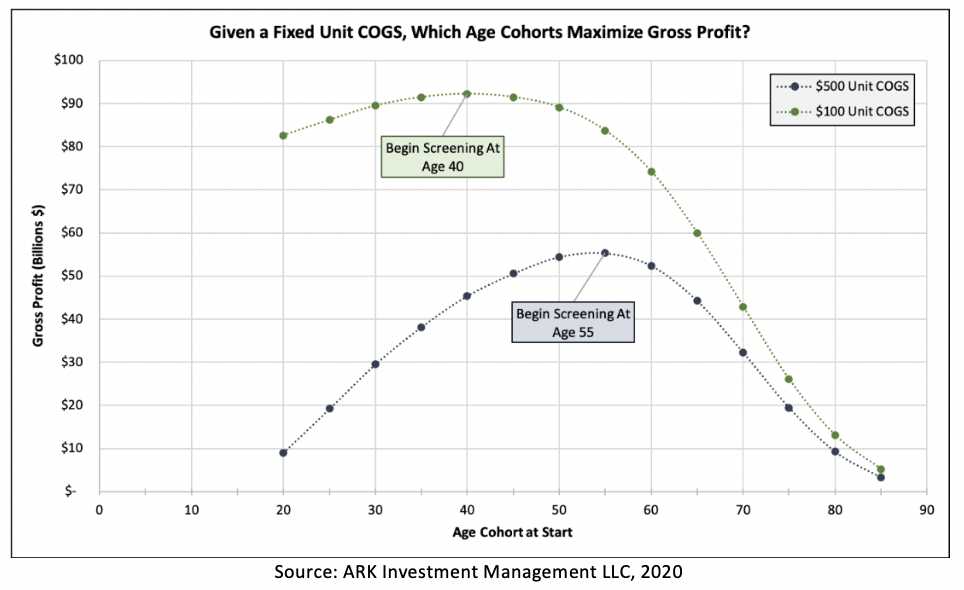

Earlier Cancer Detection with Liquid Biopsies Could Generate $50 Billion of Gross Profit

The best cancer treatment is early detection. ARK recently discussed several studies that show how non-invasive liquid biopsies have been used to detect cancer earlier. After reviewing various research studies from GRAIL, Thrive Earlier Detection, Guardant Health (GH), and Freenome, we now believe that such tests will cost somewhere between $500 and $1,500. Based on that range of cost-of-goods-sold (COGS), we have done an analysis to understand when the unit economics will be compelling enough for public and private payers to reimburse liquid biopsies.

Generally, payers reimburse medical interventions that cost $50,000 or less per quality-adjusted-life-year (QALY) added. One QALY represents a year of perfect health. Conceptually, by detecting cancer earlier, the healthcare system will recoup its upfront investment by saving on long term treatment costs and by adding QALYs. As shown in the first chart below, the unit economics of various reimbursement prices are likely to be good gauges of how rapidly health care systems will adopt liquid biopsies for earlier cancer detection. At a price point of $1,000, payers should be willing to reimburse all individuals between the ages of 55 and 85 for pan-cancer screening tests. If so, test providers with a $500 COGS should generate 50% gross margins and $50 billion in annual gross profits, as shown in the second chart below.

In the next few weeks, ARK plans to elaborate further on this opportunity and to open-source our model.

The Efficiency of AI Training Has Improved by 44x Since 2012

Computing progress is the result of compounding improvements in both hardware and software. We believe that while hardware has improved by roughly a factor of two every two years, what about software?

After analyzing neural networks from 2012 to 2019, OpenAI found that the computation necessary to train a neural network to a standard level of accuracy had dropped by a factor of 10-60x. In image recognition, modern algorithms are 44x more efficient than AlexNet, the state of the art in 2012.

ARK’s research on AI efficiency reached similar conclusions. The cost to train a neural network has dropped by roughly 10x every year, from $1,000 in the public cloud in 2017 to ~$10 today. The contributions from both hardware and software have compounded the gain, possibly explaining the more rapid rate of improvement in our results.

Sustained declines in costs can unleash successive waves of demand, creating much bigger than expected markets. According to our research, few technologies have evolved as rapidly as AI. Based on the results from these two studies, our confidence has increased that AI will have as pervasive and profound an impact as the internet.

Even in a world stuck at home, linear TV appears to be losing viewers. According to Roku, prime-time linear TV consumption in the US dropped 18% from mid-March to late April on a year over year basis. Worse yet, The Trade Desk survey results suggests that 11% of current cable subscribers, including 18% of 18-34 year-olds, will “cut the cord” by year-end. In other words, linear TV is dying.

ARK estimates that the number of linear TV households in the US will drop 48%, from 86 million today to roughly 44 million, during the next five years. In other words, the number of linear TV households will drop to a level last seen in the late 1980s, more than 30 years ago.

With fewer viewers, we believe advertising on linear TV is likely to drop 51% during the next five years, from $70 billion today to roughly $34 billion by 2025. This shift is analogous to the demise of print media during the Global Financial Crisis in 2008-2009. After levitating for years in the face of declines in readership, print advertising endured years of double-digit declines as budgets shifted to more efficient digital media formats. Print advertising never recovered; nor, in our view, will linear TV advertising.

Fintech Companies Are Approved to Distribute the Paycheck Stimulus

In the first $342 billion tranche of the Paycheck Protection Program (PPP), 68% of the 1.6 million loans originated were for more than $350,000, with the average at $206,000. In the second tranche of loans originated through May 1, only 46% of the 2.2 million were for more than $350,000, with the average down to $79,000.

In our view, the drop in average loan size in the second tranche suggests a more equitable distribution of the stimulus, aided by PayPal, Square, and other fintech companies. Validating the agility and value-add of fintech companies, the Treasury and SBA turned to them to help facilitate the second tranche of PPP loans, redressing the problems traditional banks encountered or caused during the first tranche of disbursements.

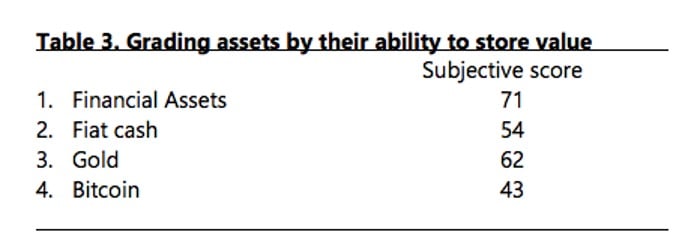

Paul Tudor Jones Makes the Case for Owning Bitcoin

In a letter to investors, macro hedge fund investor Paul Tudor Jones announced that his fund will trade bitcoin futures. Titled “The Great Monetary Inflation”, the letter makes the case for bitcoin as protection against inflation caused by the expansion of central bank balance sheets.

Comparing it to gold in the 1970s, Paul Tudor Jones views bitcoin as a strong hedge against inflation, with high appreciation potential. He and his team ranked bitcoin against cash, gold, and financial assets based on 4 characteristics:

Purchasing Power – How does this asset retain its value over time?

Trustworthiness – How is it perceived through time as a store of value?

Liquidity – How quickly can it be monetized into a transactional currency?

Portability – How easy is it to move based on unforeseen circumstances?

The scores, while subjective, were the following:

While its score was lower than the other stores of value, bitcoin’s market cap relative to its ranking is extremely low. Specifically, “Bitcoin had an overall score nearly 60% that of financial assets but has a market cap that is 1/1200th. It scores 66% of gold as a store of value, but has a market cap that is 1/60th of gold’s outstanding value.“

Could this validation provide macro hedge fund investors with the green light to invest in a new store of value, if not a new asset class?

We hope you find this information useful and please stay safe.

ARK's statements are not an endorsement of any company or a recommendation to buy, sell or hold any security. For a list of all purchases and sales made by ARK for client accounts during the past year that could be considered by the SEC as recommendations, click here. It should not be assumed that recommendations made in the future will be profitable or will equal the performance of the securities in this list. For full disclosures, click here.

You received this email because you are subscribed to Research NewslettersfromARK Investment Management LLC. Unsubscribe from ARK emails or choose the types of emails you want to receive. Unsubscribe from all.

This Newsletter is for informational purposes only and does not constitute, either explicitly or implicitly, any provision of services or products by ARK Investment Management LLC (“ARK”). Investors should determine for themselves whether a particular service or product is suitable for their investment needs or should seek such professional advice for their particular situation. All content is original and has been researched and produced by ARK unless otherwise stated therein. No part of the content may be reproduced in any form, or referred to in any other publication, without the express written permission of ARK. All statements made regarding companies, securities or other financial information contained in the content or articles relating to ARK are strictly beliefs and points of view held by ARK and are not endorsements of any company or security or recommendations to buy or sell any security. By visiting and/or otherwise using the ARK website in any way, you indicate that you understand and accept the terms of use as set forth on the website and agree to be bound by them. If you do not agree to the terms of use of the website, please do no access the website or any pages thereof. Any descriptions of, references to, or links to other products, publications or services does not constitute an endorsement, authorization, sponsorship by or affiliation with ARK with respect to any linked site or its sponsor, unless expressly stated by ARK. Any such information, products or sites have not necessarily been reviewed by ARK and are provided or maintained by third parties over whom ARK exercises no control. ARK expressly disclaims any responsibility for the content, the accuracy of the information, and/or quality of products or services provided by or advertised on these third-party sites.