Another Top Gamer Leaves Twitch

Follow Nick on Twitter @GrousARK

Michael “Shroud” Grzesiek, the second most followed streamer, is leaving Twitch to join Mixer, Microsoft’s live streaming platform. Following game-streaming’s biggest name, Tyler “Ninja” Blevins, Shroud is the second major streamer to jump from Twitch to Mixer.

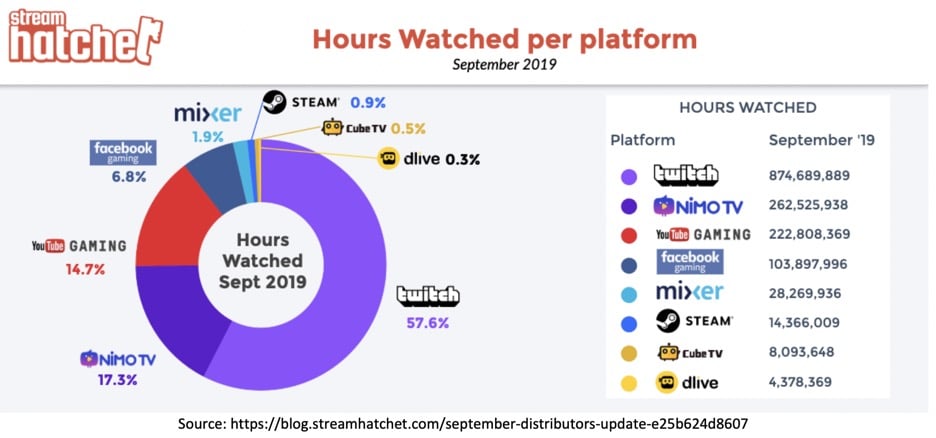

After Ninja and his 14 million followers left for Mixer, many thought that Twitch would lose some of its luster. In August, however, the month that Ninja left, Twitch outgrew its much smaller competitor with viewership up 10% sequentially compared to Mixer’s 7% gain. Ninja’s move appeared to have little to no impact on Twitch’s dominance in the game-streaming market. One reason might be the breadth of content on Twitch’s platform.

Ninja and Shroud are known for their entertaining streams of first-person shooter games like Fortnite and Apex Legends, but those games do not make up the whole market. According to Twitchtracker.com, the “All Other Games Combined” category captures 36.8% of total watched hours, suggesting relatively strong viewership across gaming and non-gaming channels that Twitch offers.

Despite the loss of Ninja and Shroud, Twitch probably will remain the leader in live game-streaming given the amount of content it offers. As shown in the chart below, Twitch accounted for 57.6% of hours viewed on global streaming platforms in September. In other words, Twitch is much bigger than the talent it hosts.

Apple Card Appears to be the Most Successful Credit Card Ever Launched

Follow George on Twitter @GeorgeOfARK

When the Apple Card launched in August, its reviews were underwhelming primarily because, unlike any other major credit offerings, it didn’t offer a signup bonus. In contrast, at its launch in August 2016, JP Morgan Chase offered a signup bonus equivalent to $1,050 in travel credits for its new credit card.

According to Google Trends, the Apple Card is extremely popular. On Goldman Sachs’ third quarter conference call, CEO David Solomon claimed that the Apple Card was the most successful credit card ever launched, appearing to validate our research. Based on Google Trends, the number of Apple Card signups in August and September was between 1.36 million and 2.04 million.

Traditionally, credit card applicants have signed up online. If approved, they would receive their credit cards in 3-5 business days and then would have to activate them either on the phone or online.

We believe one reason that the Apple Card has enjoyed rapid adoption is that Apple has reduced the number of steps and the time necessary for approval by moving the application process to the iPhone and allowing transactions immediately upon approval. As a result of Apple’s success, more fintech companies like Paypal’s Venmo are likely to offer credit cards in the coming months, adding more competitive threats to incumbent issuers.

Now Google Search Is Powered by BERT AI

Follow James on Twitter @jwangARK

A year ago, Google introduced BERT—a new kind of neural network that improved the accuracy of natural language understanding dramatically. BERT allowed AI programs to understand passages and retrieve answers with human-like accuracy. Most importantly, BERT was trained on web-scale, unlabeled data, making it far more scalable than previous approaches to artificial intelligence.

This week, Google rolled out BERT into Google Search, hailing it as one of its most important upgrades since inception. BERT will aid queries based more on sentences than keywords. When asked, “Can you pick up medicine for someone at a pharmacy?”, typically Google would return generalized pharmacy information while, now with BERT, it can understand the query and will return results relevant to picking up someone else’s medicine. Google expects that BERT will be able to handle 10% of English queries in the US, with more regions and languages added over time. Computationally intensive, BERT will leverage Google’s latest generation of cloud Tensor Processing Units (TPUs) to serve results.

As Google applies it to search, BERT is another example of AI eating traditional software. The original Google search contained little to no “AI”. Now Google Search leverages RankBrain and BERT, two deep learning-based approaches, to return results. Concurrently, it is replacing CPUs with these deep learning chips in its data centers.

While many are fearing an AI winter, in our view the AI spring has barely begun.

Square’s Cash App May Have More Monthly Active Users than Venmo

Follow Max on Twitter @mfriedrichARK

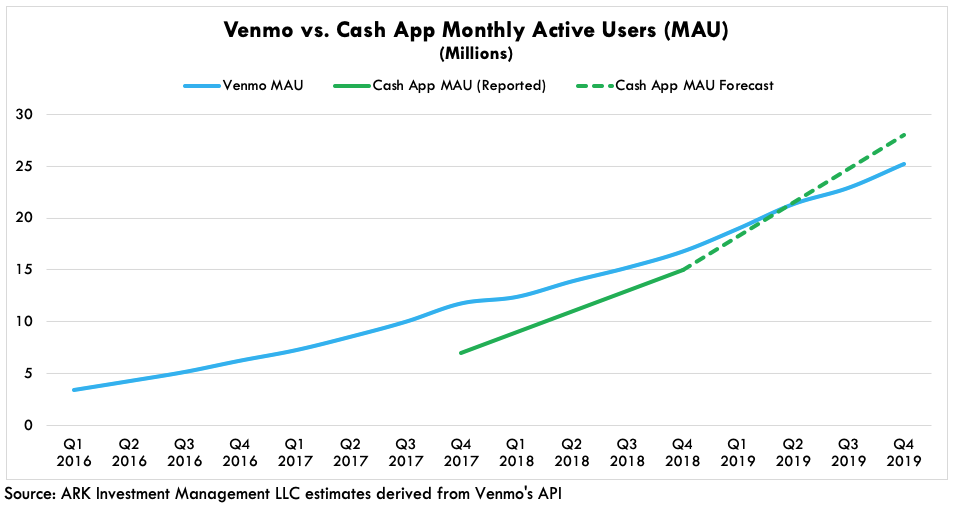

Based on data from its public API, while Venmo’s network is vibrant 10 years after its inception, 6 year old Square Cash App may have more monthly active users.

According to our research, at the end of the third quarter Venmo had 23 million monthly active users and the Cash App, more than 25 million.[1] In addition, the Cash App will end 2019 with 28 million monthly active users, up nearly two-fold from 15 million at year-end 2018, after a 115% year-over-year increase from 7 million at year-end 2017.

Cash App offers more products than does Venmo, key among the reasons that Cash App users frequent its platform more often. Cash App’s new stock trading feature also should increase user interaction. In addition, according to our research, Cash App is more popular in southern US states where un- and under-banked rates are high. According to Jack Dorsey, Square’s CEO, “People are using this as their primary bank account, and in some cases it’s their only bank account”. In other words, unlike the popular Venmo use case that splits pools for Fantasy Football, Cash App has become its users’ primary financial hub. Moreover, Cash App’s creative marketing strategy encourages users to interact with Square. Every Friday, for example, Cash App engages existing users and attracts new users with a #CashAppFriday campaign on Twitter and Instagram, collecting upwards of one million user comments. Once Cash App users post their Cash App usernames online, Square rewards some of them with dollars or bitcoin.

Read more about our analysis of Venmo’s public API data here and stay tuned for a more comprehensive report about Venmo and Cash App in the coming weeks.

Certain of the statements contained in this item may be statements of future expectations and other forward-looking statements that are based on ARK’s current views and assumptions, and involve known and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those expressed or implied in such statements.

[1] By scraping the transaction history of over 4,300 Venmo users, comprising roughly 400,000 transactions, we were able to analyze the retention characteristics and transaction frequency of quarterly Venmo user cohorts over time.

HTC Announces the First Bitcoin Full Node on Mobile

Follow Yassine on Twitter @yassineARK

Taiwanese consumer electronics company HTC has launched its highly anticipated Exodus 1s, the first smartphone capable of running a Bitcoin full node. As a result, its smartphone users will be able to validate Bitcoin transactions and blocks.

As stated by HTC’s Chief Decentralization Officer, Phil Chen, “Full nodes are the most important ingredient in the resilience of the Bitcoin network. [HTC is] providing the tools for access to universal basic finance, the tools to have a metaphorical Swiss bank in your pocket”.

The cost to run a full node often determines how decentralized a network is. By lowering the barriers to entry, HTC is enabling anyone to run a node, further decentralizing Bitcoin’s network. Along with access to a cryptocurrency hardware wallet, HTC users will be able install an SD card with enough memory and data capacity to store the full Bitcoin ledger.

While not available initially in the US, HTC will offer the Exodus 1s in 27 countries across the Middle East and Europe.