It's Monday, June 1, 2020. Please enjoy ARK's weekly newsletter curated by our thematic analysts and designed to keep you engaged with disruptive innovation.

SpaceX Makes History as the First Commercial Company to Launch Astronauts into Space

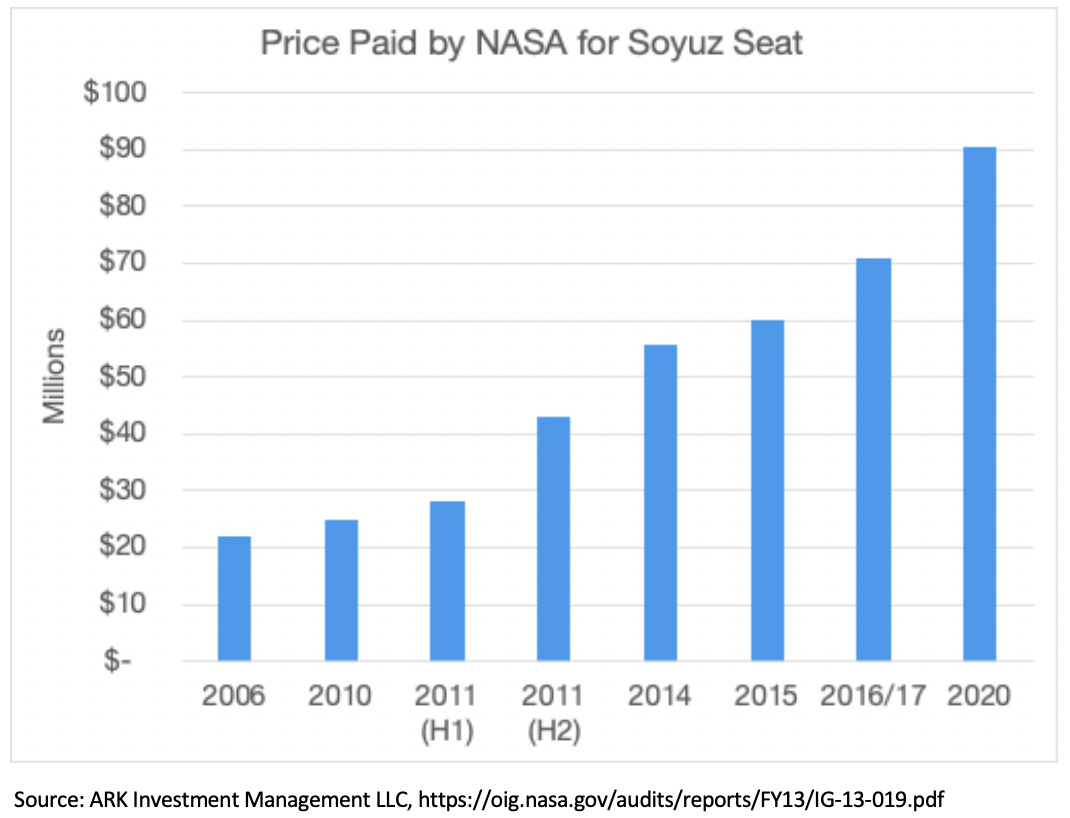

This weekend, SpaceX launched two astronauts to the International Space Station, marking the first time that a commercial aerospace company has carried humans into orbit. The US hasn’t launched its own astronauts into space since the Space Shuttle program ended in 2011, effectively holding NASA hostage to the exorbitant prices that Russia has charged to give our astronauts and cargo access to space. Since then, the price of a seat on the Russian Soyuz rocket has more than doubled from roughly $40 million to $90 million in 2020, as shown below. Apparently, SpaceX has cut the cost nearly in half to roughly $55 million.

Netflix Became HBO Faster Than HBO Could Become Netflix

Seven years ago, Netflix's Chief Content Officer Ted Sarandos stated that Netflix’s goal was "to become HBO faster than HBO can become us." That year, Netflix launched its first original show, House of Cards, marking an important turning point from its exclusive reliance on third party content. Since then, Netflix has released more original programming than any other streaming service, blowing past HBO's original content slate.

On Wednesday, HBO finally responded to Ted Sarandos' seven-year-old challenge with the release of HBO Max. Max offers more than 10,000 hours of original and third-party content for the same price as HBO Now, its original programming service. For $15 a month, HBO Max subscribers will have access to all of HBO Now’s content plus a lot more.

In ARK’s view, HBO Max’s biggest risk is distribution. At the moment, neither Roku nor Amazon Fire TV - together more than 70% of the streaming services market in the US - supports HBO MAX. Without widescale distribution, HBO Max will have a hard time catching up to Netflix.

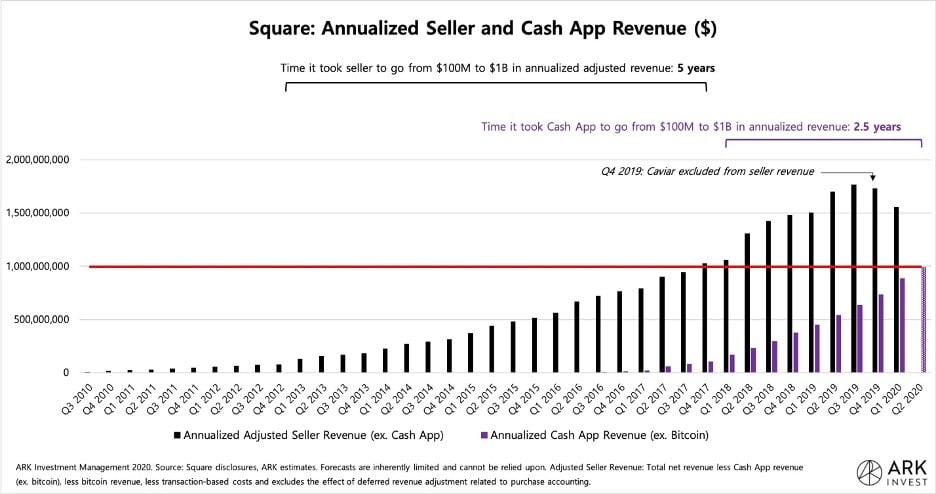

Cash App Appears to Be Growing at 2x Square’s Historical Growth Rate

While Square’s seller ecosystem grew 10-fold from $100 million to $1 billion in annualized revenue1 in five years, Cash app is likely to accomplish the same in just 2.5 years. Cash App generated roughly $100 million in annualized revenue in the fourth quarter of 2017 and is poised to eclipse $250 million, or $1 billion on an annualized basis, this quarter, as shown below.

We believe Cash App’s growth is more impressive in the absence of several monetization levers it will be able to pull in the future. Stock purchases and cross-border payments, for example, are free, and likely to follow Cash Apps’ bitcoin monetization strategy. Giving bitcoin time to penetrate Cash App’s user base, Square waited two years before charging fees for purchases. In addition, Cash App’s Instant Deposit still charges 1.5% per transaction, well below the industry average, despite sell-side analysts advocating for higher fees to boost short-term revenue growth.

Based on our five-year investment horizon, we believe that Cash App’s focus on customer acquisition first, deferring monetization until features and functions gain traction, is the right way to go.

1 Based on adjusted revenue for the seller ecosystem, which we define as total net revenue excluding Cash App revenue, bitcoin revenue, transaction-based costs, and the deferred revenue adjustment related to purchase accounting. We use adjusted revenue in this example to exclude transaction-based costs (the ~200 bps per transaction Square pays to third parties) and bitcoin revenue to arrive at the revenue from Square’s seller ecosystem.

Goldman Sachs Does Not Consider Cryptocurrencies an Asset Class

In its presentation, Goldman Sachs laid out five reasons why cryptocurrencies, including bitcoin, are not part of a new asset class. They do not:

Generate cash flow like bonds

Generate any earnings through exposure to global economic growth

Provide consistent diversification benefits given their unstable correlations

Dampen volatility

Show evidence of hedging against Inflation

ARK disagrees completely with Goldman’s assessment. As illustrated in 2016 in our white paper Bitcoin: Ringing The Bell For A New Asset Class, bitcoin exhibits the characteristics of a unique asset class. It is investable and differs substantially from other assets in its politico-economic profile, its price independence, and its risk-reward characteristics. If anything, Goldman’s observation that bitcoin does not generate cash flow or earnings reinforces why we believe it is unique: digital gold.

Goldman’s arguments against bitcoin seem stale and ill-informed. As Bloomberg editor Joe Weisenthal notes, “Goldman's anti-crypto take basically seems like a bunch of warmed-over arguments from 2014.”

According to the US Energy Information Administration, renewables exceeded coal consumption for the first time in the US in 2019. Indeed, coal consumption dropped 15% in 2019, and then another ~34% on a year over year basis in the first quarter in response to the COVID-19 related lockdown and a mild winter.

In the US today, electricity generated from coal is more expensive than that from renewables and gas. At the margin, therefore, coal should be the first energy input to decline in response to low demand while, thanks to continued cost declines, renewables displace expensive and outdated sources of electricity.

Could a Combination of Checkpoint Inhibitors Treat Solid Tumors Successfully?

When combined, immune checkpoint inhibitors (ICIs) could become successful treatments for solid tumors. The FDA already has approved two ICIs, CTLA-4 and PD-1/PD-L1. TIGIT, an early stage ICI - arguably discovered both by Genetech and Compugen - opens the possibility for more combinations. Individual Checkpoint inhibitors do not work for every cancer patient, the reason that biotech companies are conducting new combination trials.

On Friday, at the American Society of Clinical Oncology (ASCO), Genentech reported data from a combination trial with TIGIT-targeting Tiragolumab and Tecentriq, showing a 66% overall response rate for PDL1-high patients. PDL1-high refers to the amount of PDL1 proteins expressed on cancer cells. Approximately one third of front-line lung cancer patients are PDL1-high. Based on this early data, TIGIT appears to show some efficacy in the PDL1-high patient population.

We look forward to seeing more data from Genetech on the duration of therapy and the overall survival rate in this TIGIT/PDL1 ICI trial.

In Other Innovation News

NGS Assists in the Diagnosis of Rare Immunological Disorders

In collaboration with Invitae (NVTA), the Jeffrey Modell Foundation (JMF), an international patient advocacy group focused on immunological disorders, recently published the results of a genetic testing study. Highlighting the power and precision of next generation DNA sequencing (NGS) and genetic counseling, Invitae’s Primary Immunodeficiency (PI) test led to a clinical diagnosis for 45% of the patients with rare disorders. Unfortunately, 72% of the patients cited price as the reason for avoiding the test, demonstrating the importance of accelerating the push down the NGS cost curve and offering low price solutions.

Zipline Drones Take to US Skies

This week, in response to COVID-19 travel restrictions, the FAA granted drone delivery company Zipline a waiver to distribute medical equipment and supplies for Novant Health in North Carolina. ARK is staying tuned, as we believe that drones could reduce the costs of delivering food and medical supplies over a 15-mile radius to less than a dollar.

We hope you find this information useful and please stay safe.

ARK's statements are not an endorsement of any company or a recommendation to buy, sell or hold any security. For a list of all purchases and sales made by ARK for client accounts during the past year that could be considered by the SEC as recommendations, click here. It should not be assumed that recommendations made in the future will be profitable or will equal the performance of the securities in this list. For full disclosures, click here.

You received this email because you are subscribed to Research NewslettersfromARK Investment Management LLC. Unsubscribe from ARK emails or choose the types of emails you want to receive. Unsubscribe from all.

This Newsletter is for informational purposes only and does not constitute, either explicitly or implicitly, any provision of services or products by ARK Investment Management LLC (“ARK”). Investors should determine for themselves whether a particular service or product is suitable for their investment needs or should seek such professional advice for their particular situation. All content is original and has been researched and produced by ARK unless otherwise stated therein. No part of the content may be reproduced in any form, or referred to in any other publication, without the express written permission of ARK. All statements made regarding companies, securities or other financial information contained in the content or articles relating to ARK are strictly beliefs and points of view held by ARK and are not endorsements of any company or security or recommendations to buy or sell any security. By visiting and/or otherwise using the ARK website in any way, you indicate that you understand and accept the terms of use as set forth on the website and agree to be bound by them. If you do not agree to the terms of use of the website, please do no access the website or any pages thereof. Any descriptions of, references to, or links to other products, publications or services does not constitute an endorsement, authorization, sponsorship by or affiliation with ARK with respect to any linked site or its sponsor, unless expressly stated by ARK. Any such information, products or sites have not necessarily been reviewed by ARK and are provided or maintained by third parties over whom ARK exercises no control. ARK expressly disclaims any responsibility for the content, the accuracy of the information, and/or quality of products or services provided by or advertised on these third-party sites.